Moving From Rules-Based To Principles-Based Environment Little “Industry-Specific” Gaap |Impact Based On The Type Of Transactions

Foreword:

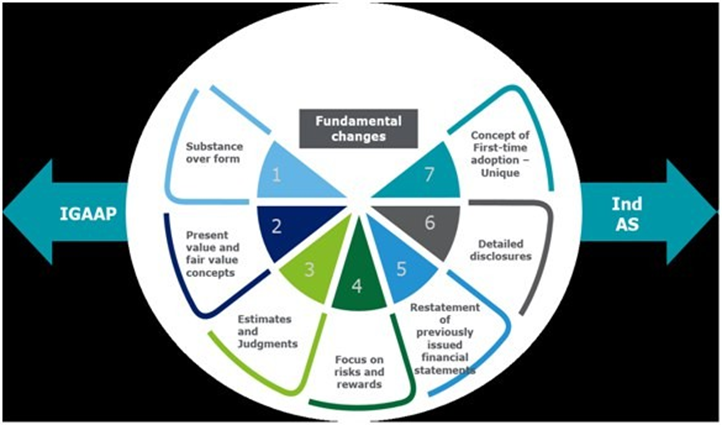

From this month we shall begin with analysing the provisions of Indian Accounting Standards (Ind AS) notified under the Companies (Indian Accounting Standards) Rules, 2015 vide Notification dated 16th February 2015 of the Ministry of Corporate Affairs (MCA).

This series will provide an overview of the accounting and key disclosure requirements prescribed by Schedule III to the Companies Act, 2013, interpretations by ICAI and the relevant clarifications provided by the Ind AS Technical Facilitation Group (ITFG) upto 31st March 2020. It will summarise the significant guidance in each standard, differences between the Act & the standard and the key amendments to the provisions of the 2013 Act notified by the MCA relevant for each standard.

LIST OF IND AS NOTIFIED TILL DATE

Till date, 41 Ind AS have been notified. The same are as under;

- Ind AS 101 – First-time adoption of Ind AS

- Ind AS 102 – Share Based payments

- Ind AS 103 – Business Combinations

- Ind AS 104 – Insurance Contracts

- Ind AS 105 – Non-Current Assets Held for Sale and Discontinued Operations

- Ind AS 106 – Exploration for and Evaluation of Mineral Resources

- Ind AS 107 – Financial Instruments: Disclosures

- Ind AS 108 – Operating Segments

- Ind AS 109 – Financial Instruments

- Ind AS 110 – Consolidated Financial Statements

- Ind AS 111 – Joint Arrangements

- Ind AS 112 – Disclosure of Interests in Other Entities

- Ind AS 113 – Fair Value Measurement

- Ind AS 114 – Regulatory Deferral Accounts

- Ind AS 115 – Revenue from Contracts with Customers

- Ind AS 1 – Presentation of Financial Statements

- Ind AS 2 – Inventories

- Ind AS 7 – Statement of Cash Flows

- Ind AS 8 – Accounting Policies, Changes in Accounting Estimates and Errors

- Ind AS 10 – Events after Reporting Period

- Ind AS 11 – Construction Contracts

- Ind AS 12 – Income Taxes

- Ind AS 16 – Property, Plant and Equipment

- Ind AS 17 – Leases

- Ind AS 18 – Revenue

- Ind AS 19 – Employee Benefits

- Ind AS 20 – Accounting for Government Grants and Disclosure of Govt. Assistance

- Ind AS 21 – The Effects of Changes in Foreign Exchange Rates

- Ind AS 23 – Borrowing Costs

- Ind AS 24 – Related Party Disclosures

- Ind AS 27 – Separate Financial Statements

- Ind AS 28 – Investments in Associates and Joint Ventures

- Ind AS 29 – Financial Reporting in Hyper inflationary Economies

- Ind AS 32 – Financial Instruments: Presentation

- Ind AS 33 – Earnings per Share

- Ind AS 34 – Interim Financial Reporting

- Ind AS 36 – Impairment of Assets

- Ind AS 37 – Provisions, Contingent Liabilities and Contingent Assets

- Ind AS 38 – Intangible Assets

- Ind AS 40 – Investment Property

- Ind AS 41 -Agriculture

Applicability

MCA had notified phase-wise adoption and applicability of the following Ind AS for companies as under:

| MCA roadmap to Ind AS for all companies except banks, Non-Banking Financial Company (NBFCs), and insurance companies | |

| 2015-16 Voluntary adoption | Early adoption |

| 2016-17 Phase I | Companies with net worth of Rs.500 crores or more |

| 2017-18 Phase II | All listed companies not covered aboveAll unlisted companies with net worth of Rs.250 crores or more |

| MCA roadmap to Ind AS for banks, Non-Banking Financial Company (NBFCs), and insurance companies | |

| 2018-19 Phase I | Scheduled commercial banks, Term-lending refinancing institutions Insurer/insurance companies NBFC with net worth of Rs.500 crores or more |

| 2019-20 Phase II | All listed NBFC’s (or in the process of listing) and not covered in Phase I above All unlisted NBFCs with net worth of Rs.250 crores or more but less than 500 crores |

- The above road map also applies to the Holding, subsidiary, joint venture or associate companies of the listed and unlisted companies covered above.

Ind AS Technical Facilitation Group (ITFG) has provided certain clarifications for the issues raised on the applicability of Ind AS listed as below:

Issue 2:

Applicability of Ind AS to a branch of a company incorporated outside India

Q – Will Ind AS be applicable to a Co. incorporated outside India with limited liability, having established a branch office in India with RBI permission to provide consultancy service?

A – Ind AS road map is applicable to a company as defined in section 2(20) of the 2013 Act. Since as per the definition, a branch office of a foreign company does not meet the definition of a company as per 2013 Act, Ind AS is not applicable to a branch of the company not incorporated in India. (Ref – Issue 6 – Bulletin 12 of ITFG).

Issue 3:

Applicability of Ind AS to entities in a group

A listed entity (B), was covered under the 2nd phase of the IND AS corporate road map.

- Company A (unlisted company with net worth less than 250 crore), holding company of B: Holding, subsidiaries, associate and joint venture companies of the entities covered in the IND AS corporate road map will be covered. Accordingly, Company A will be required to prepare Ind AS financial statements.

- Company C (unlisted company with net worth less than 250 crore), fellow subsidiary of B (subsidiary of A):

ITFG noted that the requirement to adopt Ind AS does not extend to fellow subsidiary of a holding company which is required to adopt Ind AS because of its holding company relationship with a subsidiary meeting the net worth / listing criteria. However, company C will be required to furnish Ind AS financial statements for the purpose of A’s consolidation. Hence company C may voluntarily opt to prepare Ind AS financial statements for the purpose of statutory reporting.

- Company D (unlisted company with net worth less than 250 crore), an investor take holds 25% stake in B:

An investor company does not qualify as holding company of B. Therefore, company D is not required to comply with Ind AS by virtue of company B falling under the threshold of Ind AS applicability. However, for consolidation purpose of company B, company B will have to prepare financials statements in accordance with Companies (Accounting Standard) Rules, 2006 for which company D has to prepare its financials as per these rules. (Ref – Issue 10 – Bulletin 15 ITFG)

Issue 3:

Applicability of Ind AS to a group

Q – Parent (ABC Ltd) and its unlisted subsidiary (PQR Ltd – with net worth of INR 50cr) complied with IND AS beginning 1st April 2019 considering the requirements of road map. During financial year 2020-21, ABC Ltd sold off substantially all its investments in PQR Ltd to an unrelated unlisted company, XYZ Ltd. Will PQR Ltd and XYZ Ltd be required to apply Ind AS after its substantial sale of its shareholding?

A – ITGF clarified that PQR Ltd is required to continue preparing financial statements as per Ind AS considering the requirement of Rule 9 of Ind AS Rules which provide that once a company adopts Ind AS either voluntarily or mandatorily, it would be required to continue comply Ind AS for all the subsequent years.

XYZ Ltd is the holding company of PQR Ltd. XYZ Ltd, does not meet the specified criteria (either the net worth or the listing criteria) of the Ind AS road map. Ind AS does not apply to XYZ Ltd simply by the virtue of being PQR’s parent. However, it may opt to apply Ind AS voluntarily. (Ref – Issue 6 – Bulletin 19)

FIRST TIME ADOPTION OF IND AS 101

Ind AS 101 applies to the 1st Ind AS compliant financial statements and the interim reports presented under Ind AS 34, ‘Interim financial reporting’which are part of that period, prepared by the entity.

This Ind AS establishes two categories of exceptions to the principle that an entity’s opening Ind AS BalanceSheet shall comply with each Ind AS:

- Paragraphs 14–17 and Appendix B prohibit retrospective application of some aspects of other Ind ASs.

- Appendices C–D grant exemptions from some requirements of other Ind AS

Comparative Information

Entity’s 1st Ind AS financial statement should include:

- Three balance sheets (including an opening balance sheet

- Two statements of profit and loss

- Two statements of cash flows

- Two statements of changes in equity and

- Related notes for all statements presented

Explanation of Transition to Ind AS

Detailed disclosure on how the transition from GAAP to Ind AS on the first time adoption of Ind AS needs to be provided. An opening balance sheet is prepared at the date of transition along with one year of comparatives presented on the basis of Ind AS.

Reconciliations

To comply with the need for furnishing an Explanation of transition to Ind AS, an entity’s first Ind AS financial statements shall include:

- The reconciliations of its equity reported in accordance with previous GAAP to its equity in accordance with Ind AS,

- A reconciliation to its total comprehensive income in accordance with Ind ASs for the latest period in theentity’s most recent annual financial statements, and

- If the entity recognised or reversed any impairment losses for the first time in preparing its opening Ind ASBalance Sheet, the disclosures that Ind AS 36, Impairment of Assets, would have required if the entity hadrecognised those impairment losses or reversals in the period beginning with the date of transition to Ind AS.

On 30 March 2019, MCA notified Appendix C to Ind AS 12, providing clarification on the accounting of income taxes in case of uncertainty over a certain income tax treatment. The amendment to Ind AS 101, clarifies that when the date of transition to Ind AS is before the date of notification of Appendix C, then the first time adopter of Ind AS may elect to recognise the cumulative effect of applying Appendix C as an adjustment to the opening balance of retained earnings at the beginning of the Ind AS reporting period.

Accounting Policies

The accounting policies adopted under GAAP should be consistent at the time of adoption of Ind AS. Unless there is any adjustments made retrospectively to the retained earnings that arise from events and transactions as a result of difference between the GAAP and Ind AS. However, there are a number of optional exemptions and mandatory exceptions to the requirement of retrospective application.

The optional exemptions relate to the following:

- Share-based payment transactions

- Insurance contracts

- Deemed cost

- Leases

- Cumulative translation differences

- Investment in subsidiaries, joint ventures and associates

- Assets and liabilities of subsidiaries, joint ventures andassociates

- Compound financial instruments

- Designation of previously recognised financial instruments

- Fair value measurement of financial assets or financial

- liabilities at initial recognition

- Decommissioning liabilities included in the cost of property,plant and equipment

- Financial assets or intangible asset accounted for inaccordance with service concession arrangement

- Borrowing costs

- Extinguishing financial liabilities with equity instruments

- Severe hyperinflation

- Joint arrangements

- Stripping costs in the production phase of a surface mine

- Designation of contracts to buy or sell a non-financial item

- Revenue from contracts with customers (Ind AS 115)

- Non-current assets held for sale and discontinued operations

Further, there are mandatory exceptions in applying the Ind AS requirements as summarised below:

- De-recognition of financial assets and liabilities

- Hedge accounting

- Non-controlling interests

- Classification and measurement of financial assets

- Impairment of financial assets

- Embedded derivatives

- Government loans

- Estimates

Significant carve – outs from IFRS

India has chosen a path of International Financial Reporting Standards (IFRS) convergence rather than adoption. Hence, Ind AS are primarily based on the IFRS issued by the International Accounting Standards Board (IASB). However, there are certain carve-outs from the IFRS.

a) Presentation of comparatives in the First-time Adoption of Indian Accounting Standards (Ind AS) 101 (Corresponding to IFRS 1)

IFRS 1 defines transitional date as beginning of the earliest period for which an entity presents full comparative information under IFRS. It is this date which is the starting point for IFRS and it is on this date the cumulative impact of transition is recorded based on assessment of conditions at that date by applying the standards retrospectively except to the extent specifically provided in this standard as optional exemptions and mandatory exceptions. Accordingly, the comparatives, i.e., the previous year figures are also presented in the first financial statements prepared under IFRS on the basis of IFRS.

Carve Out

Ind AS 101, requires an entity to provide comparatives as per the existing notified Accounting Standards. It is provided that, in addition to aforesaid comparatives, an entity may also provide comparatives as per Ind AS on a memorandum basis.

b) Presentation of Reconciliation

IFRS 1 requires reconciliations for opening equity, total comprehensive income, cash flow statement and closing equity for the comparative period to explain the transition to IFRS from previous GAAP.

Carve Out

Ind AS 101 provides an option to provide a comparative financial statement on memorandum basis. Where the entities do not exercise this option and, therefore, do not provide comparatives, they need not provide reconciliation for total comprehensive income, cash flow statement and closing equity in the first year of transition but are expected to disclose significant differences pertaining to total comprehensive income. Entities that provide comparatives would have to provide reconciliations which are similar to IFRS.

c) Cost of Non-current Assets Held for Sale and Discontinued Operations on the date of Transition on First-time Adoption of Indian Accounting Standards (Ind AS)

Carve Out

Ind AS 101 provides transitional relief that while applying Ind AS 105 – Non-current Assets Held for Sale and Discontinued Operations, an entity may use the transitional date circumstances to measure such assets or operations at the lower of carrying value and fair value less cost to sell.

d) Foreign Currency Gains/Losses on Translation of Long Term Monetary Items Carve out

Ind AS 101 provides that on the date of transition, if there are long-term monetary assets or long-term monetary liabilities mentioned in Ind AS 21, an entity may exercise the option mentioned regarding spreading over the unrealised Gains/Losses over the life of Assets/Liabilities either retrospectively or prospectively. If this option is exercised prospectively, the accumulated exchange differences in respect of those items are deemed to be zero on the date of transition.

e) Financial Instruments Existing on Transition Date Carve out

Ind AS 101 provides that the financial instruments carried at amortised cost should be measured in accordance with Ind AS 39 from the date of recognition of financial instruments unless it is impracticable

(as defined in Ind AS 8) for an entity to apply retrospectively the effective interest method or the impairment requirements of Ind AS 39. If it is impracticable to do so then the fair value of the financial asset at the date of transition to Ind-ASs shall be the new amortised cost of that financial asset at the date of transition to Ind ASs. Ind AS 101 provides another exemption that financial instruments measured at fair value shall be measured at fair value as on the date of transition to Ind AS.

f) Definition of Previous GAAP Under Ind AS 101 First time Adoption of Indian Accounting Standards

IFRS 1 defines previous GAAP as the basis of accounting that a first-time adopter used immediately before adopting IFRS.

Carve out

Ind AS 101 defines previous GAAP as the basis of accounting that a first-time adopter used immediately before adopting Ind ASs for its reporting requirements in India. For instance, for companies preparing their financial statements in accordance with the existing Accounting Standards notified under the Companies (Accounting Standards) Rules, 2006 shall consider those financial statements as previous GAAP financial statements. g) Cost of Property, Plant and Equipment (PPE), Intangible Assets, Investment Property, on the Date of Transition of First-time Adoption of Indian Accounting Standards Ind AS 101 provides an entity an option to use carrying values of all assets as on the date of transition in accordance with previous GAAP as an acceptable starting point under Ind AS.

To conclude, first time adopter is an entity that presents its 1st Ind AS financial statements. ITFG has provided clarification on specific issues which will be covered with the specific Ind AS in the following months. Comparative information is prepared and presented on the basis of Ind AS. Almost all adjustments arising from the first-time application of Ind AS are adjusted against opening retained earnings (or, if appropriate, another category of equity) of the first period that is presented on an Ind AS basis. Disclosures of certain reconciliations from Indian GAAP to Ind AS are required. Next month, we shall cover further Ind AS.