DETAILED ANALYSIS OF SECTION 185 & 186 OF THE COMPANIES ACT, 2013

summarise sections 185 & 186 and understand the provision of relevant acts

- Section 185 of Companies Act,2013 – Whether Loan, advance or guarantee is allowed to Directors or other.

- Section 186 of Companies Act, 2013 – If Loan and investment by company is allowed as per section 185 & Section 2(22)(e) then what will be limit to the extent of which Loan & Investment will be allowed under section 186.

Detail Analysis of these sect0069ons

Part I

Section 185 – Loan to Directors

Company shall not provide loan to director/ partner or relative of such director/ any firm in which such director or relative is partner/Director of Its holding co.

- No company shall, directly or indirectly, advance any loan, including any loan represented by a book debt to, or give any guarantee or provide any security in connection with any loan taken by, —

- any director of company, or

- Director of a company which is its holding company or

- any partner or relative of any such director; or

- any firm in which any such director or relative is a partner.

Note: – What is an indirect loan is not defined in section 185 or elsewhere in the Act. Indirect loan is interpreted in case of Dr. Fredie Ardeshir Mehta v. Union of India [1991] 70 Comp. Cas. 210 (Bom.)

Company may provide loan to borrowing company if some conditions are satisfied

- A company may advance any loan including any loan represented by a book debt, or give any guarantee or provide any security in connection with any loan taken by any person in whom any of the director of the company is interested, subject to the condition that—

- a special resolution is passed by the company in general meeting:

Provided that…

the explanatory statement to the notice for the relevant general meeting shall disclose the full particulars of the loans given, or guarantee given or security provided and the purpose for which the loan or guarantee or security is proposed to be utilised by the recipient of the loan or guarantee or security and any other relevant fact; and

- The loans are utilised by the borrowing company (recipient) for its principal business activities.

Note: –In clause (b) of Section 185(2) word “Company” deliberately used because in explanation of any person define itself Applicability on Companies

Explanation —For the purposes of this sub-section, the expression “any person in whom any of the director of the company is interested” means—

(a) any private company of which any such director is a director or member;

(b) any body corporate at a general meeting of which not less than 25%. of the total voting power may be exercised or controlled by any such director, or by two or more such directors, together; or

(c) any body corporate, the Board of directors, managing director or manager, whereof is accustomed to act in accordance with the directions or instructions of the Board, or of any director or directors, of the lending company.

Non- Applicability of Section 185

- Nothing contained in sub-sections (1) and (2) shall apply to—

- The giving of any loan to a managing or whole-time director—

i) as a part of the conditions of service extended by the company to all its employees; or

ii) pursuant to any scheme approved by the members by a special resolution; or

- A company which in the ordinary course of its business provides loans or gives guarantees or securities for the due repayment of any loan and in respect of such loans an interest is charged at a rate not less than the rate of prevailing yield of one year, three years, five years or ten years Government security closest to the tenor of the loan; or (like Banking Companies, NBFC).

If the loans made under clauses (c) and (d) are utilised by the subsidiary company for its principal business activities, then section will not applicable otherwise will applicable.

- Any loan made by a holding company to its wholly owned subsidiary company or any guarantee given or security provided by a holding company in respect of any loan made to its wholly owned subsidiary company; or

- Any guarantee given or security provided by a holding company in respect of loan made by any bank or financial institution to its subsidiary company:

Note:- Limitation given above under First proviso to section 185 (3) is applicable for Subsidiary company where loan provided by holding company. However, such limitation is not applicable where loan is provided by Subsidiary company to its Holding company under this sub-section.

Contravention of this section is a punishable offence

- If any loan is advanced or a guarantee or security is given or provided or utilised in contravention of the provisions of this section, —

| Liability of | Fine | Imprisonment | both |

| Company | Minimum ₹ 5 lakh. Maximum ₹ 25 lakh | NA | NA |

| every officer of the company who is in default | Minimum ₹ 5 lakh. Maximum ₹ 25 lakh or | for a term Maximum 6 months | NA |

| the director or the other person to whom any loan is advanced or guarantee or security is given or provided in connection with any loan taken by him or the other person | Minimum ₹ 5 lakh. Maximum ₹ 25 lakh or | for a term Maximum 6 months | Or with both |

Illustrations of loan to directors:

Examples shared in below table depicts certain real life practical situations related to Section 185 and how they should be dealt with.

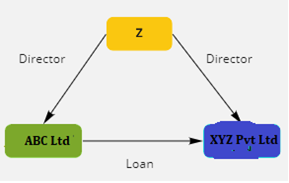

Issue 1:

Z is a director in ABC Ltd and also in XYZ Pvt Ltd. Can ABC Ltd give loan to XYZ Pvt Ltd?

Ans: XYZ Pvt Ltd will be treated as person in whom director is interested. Loan can be given after passing Special Resolution.

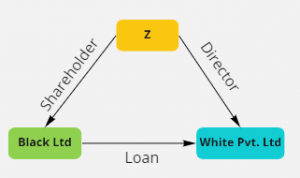

Issue 2:

Black Ltd grants loan to White Pvt Ltd. Z is a shareholder of Black Ltd and a director in White Pvt Ltd.

Ans: Allowed. As this transaction is not covered under Section 185.

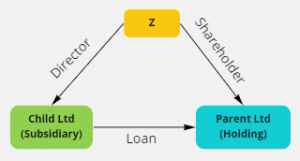

Issue 3:

Child Ltd (subsidiary Co.) grants loan to Parent Ltd. (Holding Co.) Z is Director of Child Ltd and shareholder of Parent Ltd.

Ans: Allowed. As this transaction is not covered under Section 185

Part II

Section 186 – Loan and investment by company.

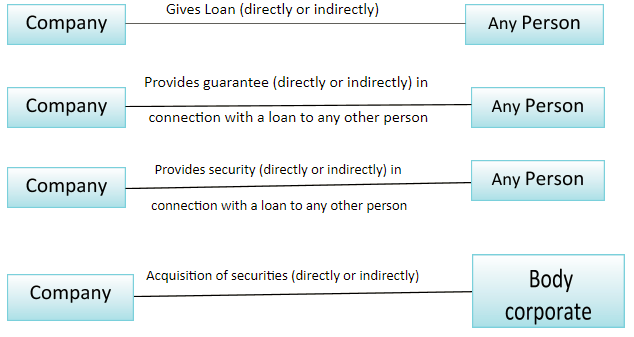

No company shall directly or indirectly—

(a) give any loan to any person or other body corporate;

(b) give any guarantee or provide security in connection with a loan to any other body corporate or person; and

(c) acquire by way of subscription, purchase or otherwise, the securities of any other body corporate,

exceeding 60% of its paid-up share capital, free reserves and securities premium account or 100% of its free reserves and securities premium account,

whichever is more.

Legal requirements:

Requirement No. 1: Approval of Board

- The approval of the Board is required in all cases irrespective of the amount of loan, investment, guarantee or security.

- The approval of the Board shall be obtained by means of a unanimous resolution passed at a Board meeting with the consent of all the directors present at the meeting.

- Resolution by circulation or resolution of the committee of directors is not sufficient.

Requirement No.2: Approval of the members by passing Special Resolution

- When the aggregate of the loan, investment, guarantee or security already made together with the loan, investment, guarantee or security proposed to be made exceeds the limit specified u/s 186(2), prior approval by means of a special resolution is necessary.

- Limit u/s 186(2) is higher of –

60% of (paid-up share capital + free reserves + securities premium) or

100% of (free reserves + securities premium).

- The contents of the Special resolution shall contain the total amount up to which the Board is authorized to make loans, guarantee, investment or security.

- No approval by way of SR is required, where –

- The loan is given by a company to its Wholly Owned Subsidiary [WOS] or joint venture company [JVC], or

- The guarantee is given or security is provided by a company to its WOS or JVC.

- Where the acquisition of securities of its wholly owned subsidiary is made by a holding company, by way of subscription or otherwise.

Requirement No.3: Approval of public financial institution [PFI]

- The company shall obtain the prior approval of PFI from which it has taken a term loan.

- Approval of PFI is not required if –

- The aggregate of loans, guarantee, investments or security already made together with the loan, investment, guarantee or security proposed to be made does not exceed the limit given.

- There is no default in repayment of loan installments or interest to PFI as per the terms and conditions of such term loan.

Requirement No.4: Rate of interest

The rate of interest chargeable should be more than the prevailing yield of Government Security closest to the period of the loan.

Requirement No.5: No subsisting default with respect to deposits

- A company which has defaulted in repayment of any deposits accepted by it or in payment of interest on deposits, shall not make any loan, guarantee, investments or security till such default is subsisting.

- In other words, where a company fails to repay the deposits or interest thereon on the due date, it may make loan, guarantee, investments or security only after the default has been made good.

Requirement No.6: Disclosures in financial statements

The company shall disclose to the members in the financial statement –

- The full particulars of any loans given, investments made, guarantee or security provided, and

- The purpose for which the loan or guarantee or security is proposed to be utilized by the recipient.

Non-applicability of Section 186

With respect to Government Company

- A Government company engaged in defense production.

- A Government company, other than a listed company, in case such company obtains approval of the Ministry or Department of CG which is administratively in charge of the company or State Government, as the case may be.

With respect to the acquisition of shares

- Any acquisition of shares allotted in pursuance of right shares.

- Any acquisition made by a company whose principal business is the acquisition of securities (i.e. investment company).

With respect to loans, guarantee or security

- A banking company in the ordinary course of its business;

- An insurance company in the ordinary course of its business;

- A housing finance company in the ordinary course of its business;

- A company engaged in the business of financing of companies or of providing infrastructural facilities.

With respect to the acquisition of shares and loan

- Any acquisition made by a non-banking financial company whose principal business is the acquisition of securities.

- The exemption to NBFC shall be with respect to investment and lending activities.

Penalty For Contravention Of Section 186

| Liability of | Fine | Imprisonment | both |

| Company | Minimum ₹ 5 lakh. Maximum ₹ 25 lakh | NA | NA |

| every officer of the company who is in default | Minimum ₹ 5 lakh. Maximum ₹ 25 lakh or | May extend to 2 years | NA |

Explanation.—For the purposes of this sub-section, the word “person” does not include any individual who is in the employment of the company.

Conclusion – From provision to analysis we can conclude that If section 185 of Companies Act, 2013 is invoked i.e. Non-Compliance of this section then such non-compliance have to be report under the notes to account as an Related party transaction of the Financial statements of the company and Statutory Auditor of the company will provide qualified opinion and will disclose in its audit report as well as where CARO, 2020 [Paragraph 3(iv)] will applicable on the company then also such disclosure will be required.

Company and its Directors and Officers may also be liable for offence by way penalty or imprisonment as the case may be given u/s 185(4) of the Companies Act, 2013.

Disclaimer: The information given in this document has been made on the basis of the provisions stated in the Companies Act, 2013. It is based on the analysis and interpretation of applicable laws as on date. The information in this document is for general informational purposes only and is not a legal advice or a legal opinion. You should seek the advice of legal counsel of your choice before acting upon any of the information in this document.