OPERATING LEVERAGE – A DOUBLE-EDGED SWORD

Ever thought, why are commodity stocks (eg: steel sector) doing so well? What if all of a sudden, the companies that we’re invested in start generating higher topline (with no growth capex), how much wealth would it create for its shareholders? Well, it turns out, it’s not as easy as it looks. Why? The answer to it is Operating Leverage.

What is Operating Leverage?

Operating Leverage (OL) measures change in operating profit with change in topline. OL explains how risky, volatile and swinging can a company’s operating profit can be.

Changes in topline can happen for two reasons:

- Change in sales price or/and

- Change in sales quantity

What is Degree of Operating Leverage?

The Degree of Operating Leverage (DOL) is a method used to quantify a company’s operating risk. DOL ranges from -1 to 1. This risk is nothing but change in operating profit arisingdue to:

- Change in topline and

- Contribution ratio (sales – variable costs)

- This assumes the fact that fixed costs are constant for any number of units sold.

How does DOL affect operating profit?

Like discussed above, change in topline can happen for two reasons:

- Change in sales price:

The delta in operating profit (also called as DOL) due to change in salesprice is -1 or +1, which means entire change in topline due to change in sales price is captured in the operating profit.

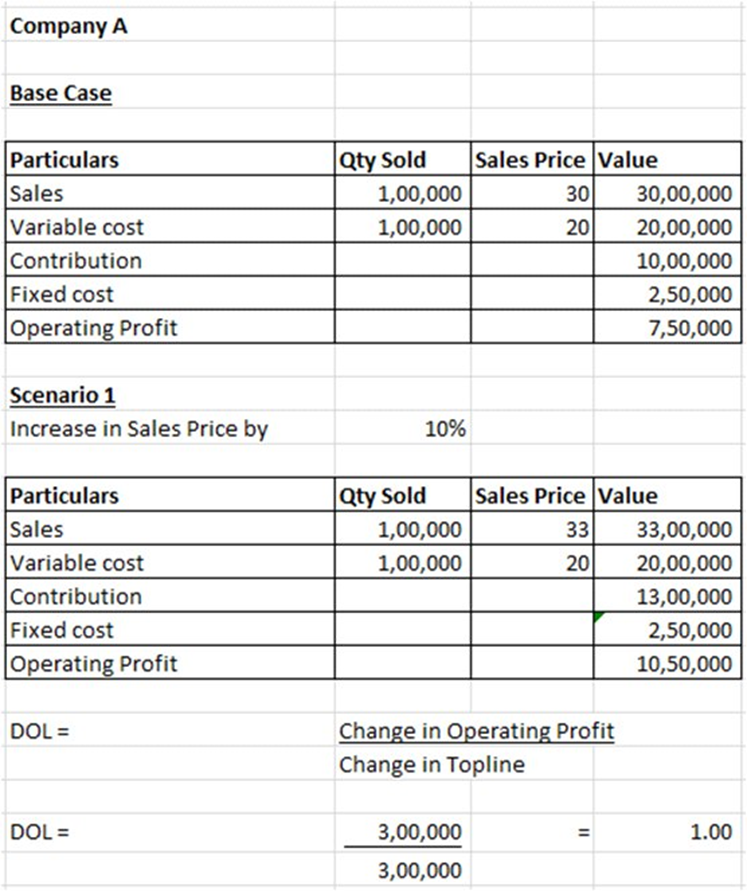

Let’s assume Company A is operating in commodity business (say a steel sector).

You can corelate this with steel companies selling at 54000/tonnetoday v/s selling at 38000/tonne six months back. Entire incremental 16000/tonne (sales) gets directly added to the profitability, everything else remaining the same, due to DOL being 1.

- Change in sales quantity:

The delta in operating profit (DOL) due to change in sales quantity depends upon the contribution ratio, which means entire change in topline due to change in sales quantity is captured in the operating income to the extent of contribution ratio.

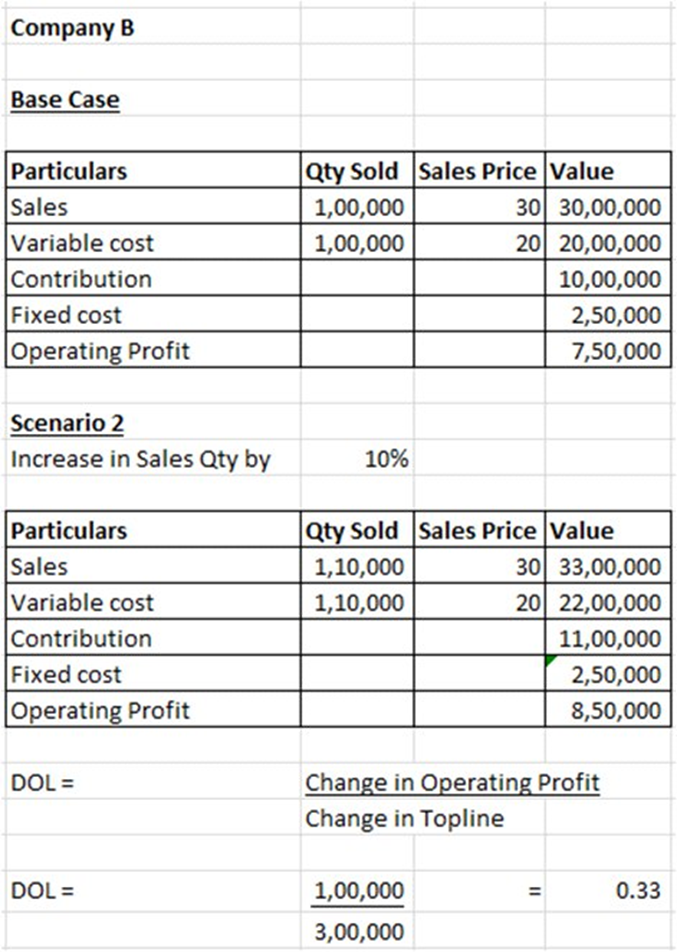

Let’s assume Company B is operating in FMCG business (say selling toothpaste).

You can corelate this with a company increasing utilization levels up from say a 70% to 80%. Entire incremental sales DOESNOT get added to the profitability, due to DOL being less than 1.

From the above two scenarios we can conclude that higher DOL exists for scenario 1 due to change in sales price.

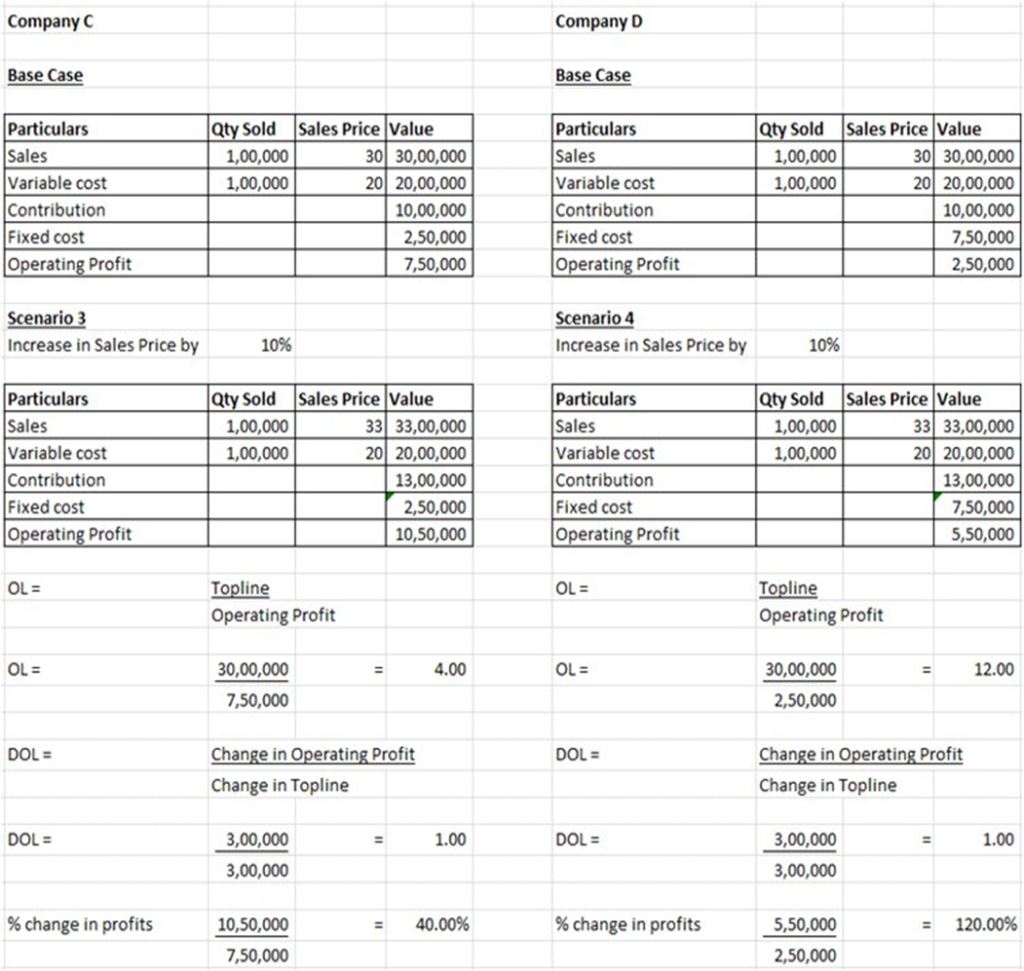

Now let us compare a scenario of two companies operating in the same sector (having same contribution ratio), but having a different fixed cost structure.

Let’s assume Company C and Company D are operating in commodity business (say a steel sector).

DOL is same (due to similar contribution ratio), but % change in profits is more for the company having higher fixed costs implying that recovery in profits in absolute terms is the same, but relatively it’s much more for Company D as compared to Company C.

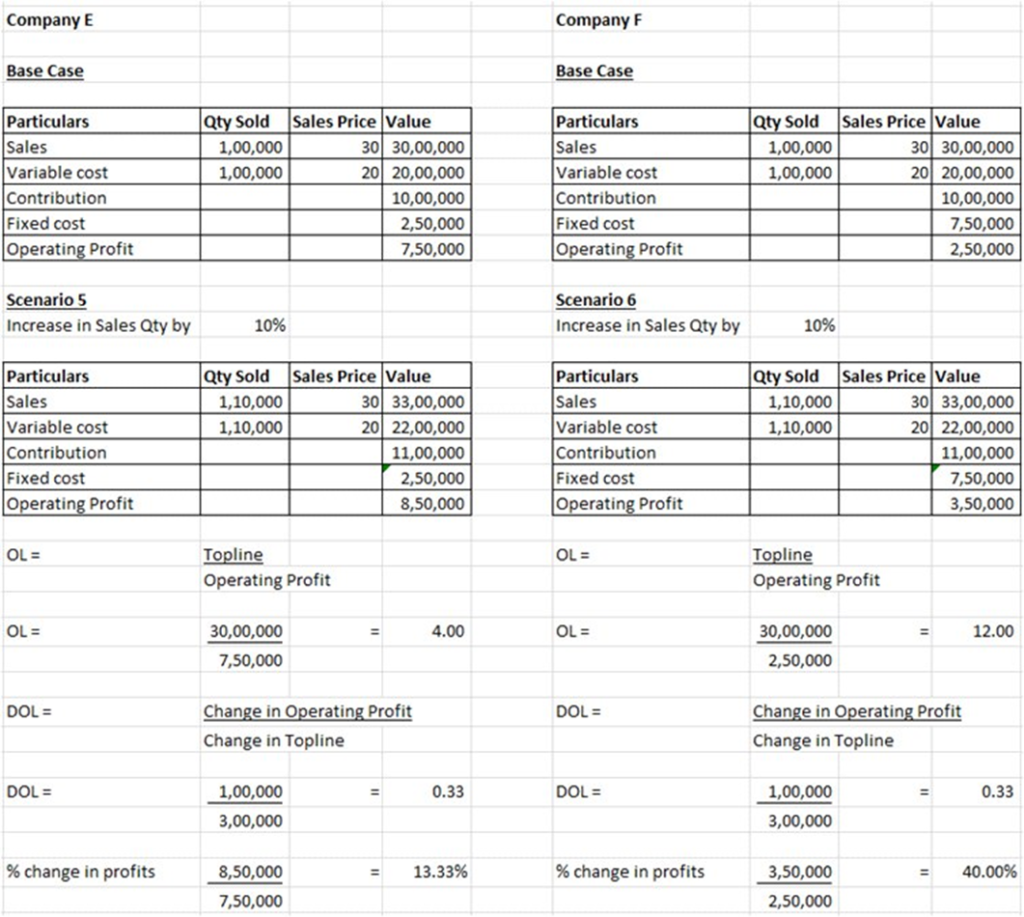

Let’s assume Company E and Company F are operating in FMCG business (say selling toothpaste).

OL is same (due to similar contribution ratio), but % change in profits is more for the company having higher fixed costs implying that recovery in profits in absolute terms is the same, but relatively it’s much more for Company E as compared to Company F.

This change in improvement of profits looks bigger and better due to impact of OL.This % improvement looks bigger for Company D as compared to Company F, due to higher DOL.In other words, companies with higher DOL and higher fixed costs show drastic movements (eg: SAIL).

In good times, OL can supercharge profit growth. In bad times, it can crush profits. Even a rough idea of a company’s operating leverage can tell you a lot about a company’s prospects.

Higher DOL with higher fixed cost structure is the most lethal combination of Operating Leverage.

How to take benefit and find opportunities in OL as an investment theme?

- DOL ranges from -1 to +1 and the sensitivity of the earning are higher near both the ends of the range.

- To take benefit of +1 DOL, it is important to remain invested at or near the bottom of the cycle, from where the entire upcycle can be ridden.

- These opportunities exist massively in commodity markets which are cyclical in nature

- Being cognizant of “point in cycle” helps youposition well.

- Cost sheet with higher fixed cost (Company D &Company F) will be extremely volatile and may results in higher delta in stock price movements too.

- Look for companies with low-capacity utilizations, where capex is already doneand volumes are yet to come in. Market should not be pricing in these volumes when you are buying it.

- Valuations of investments at the start of the uptick of the earnings is dirt cheap and hence OL massively increases earnings and hence increases valuation multiple too. Reverse is true, when timed wrong.

- OL can be your best friend if played well.

How to avoid a trap in OL?

- Firstly, knowledge about knowing that your investments have OL, is a half battle won.

- It is important to NOT ride the journey with -1 DOL. This will just more than halve your investment in no time .

- Without any scope of a material change in sales quantity (ignoring any scope of change in sales price too), it brings a lot of risk into buying a “VALUE TRAP” investment if timed badly.

- Ability to imagine a reversal of earnings cycle.

- Being cautious about momentum or chasing the sector when its already heated up.

- OL can be your worst enemy if NOT played well.

How will OL fare with any other normal investment?

- OL is a play within company’s existing set up; while your other investments will most probably be growth stories, requiring companies to scale up.

- OL bring a lot of volatility with poor earnings visibility and hence poor valuations.

- OL plays may not be big multi-baggers, they WILL have limitations at some point in time.

- If timed well, OL can be a low-risk high return investment

- OL requires you to TIME the markets; while other growth investment stories don’t require this skill.

- Capability to handle and manage volatility is the key skill set to play OL.

In the entire discussion above, we have excluded change in variable costs which also is a part of the concept of OL. This is just to make our discussion little easier to understand. Because many businesses do have variable costs swinging up and down from 10% to 200%, which brings out more volatility and highly poor earnings visibility and hence more challenging to analyze.

With all said and done, can we find an opportunity in the markets by our understanding of OL? Yes, why not! But remember one thing, as we titled it, OL is a double-edged sword. Use it to your favor and don’t let it kill you.