Resolving Dual Tax Residency: Interplay of Domestic Law and Treaty Frameworks

- Introduction

- In recent years, increased global mobility and cross-border business activities have significantly expanded the tax exposure of individuals and entities across multiple jurisdictions. As countries adopt differing criteria to determine tax residency—such as physical presence, domicile, citizenship, place of incorporation, or place of effective management—it has become increasingly common for a person to qualify as a tax resident in more than one jurisdiction.

- This phenomenon, commonly referred to as dual residency (DR), arises when a person—whether an individual or a legal entity—is regarded as a tax resident under the domestic laws of two jurisdictions simultaneously. Such situations give rise to significant challenges, including the possibility of the same income being taxed in multiple jurisdictions and increased compliance complexities in determining treaty eligibility and foreign tax credit.

- Given the fundamental role of tax residency in determining tax liability, it is essential to first understand how residency is determined under domestic law and its interaction with income taxation.

2. Interplay of domestic residency and income taxation

- Indian Tax residency Provisions

Sec 6 of the Income Tax Act (‘ITA’) 2025 provides the framework for determining the residential status of a person. The key provisions are summarized below:

- A Company is resident in India if:

- It is an Indian company or

- its place of effective management is in India i.e. where key management and commercial decisions necessary for the conduct of business are, in substance, made.

- In case of any other person (other than individuals)

- residence in India is presumed unless control and management of affairs is wholly exercised outside India.

- Individuals are classified as:

- Resident and Ordinarily Resident (ROR)

- Resident but Not Ordinarily Resident (NOR)

- Non-Resident (NR)

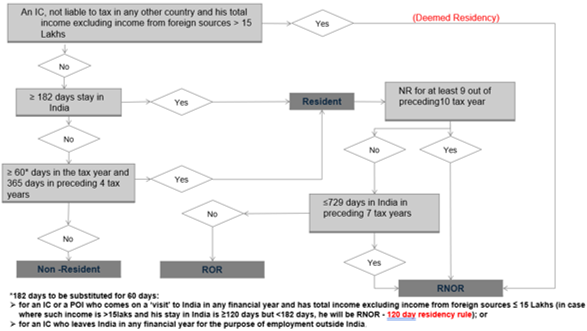

- The NOR category provides transitional relief to individuals with limited economic presence in India, thereby restricting the scope of income taxable in India. A threshold of 182 days was provided to an India Citizen (‘IC’) or Person of Indian Origin(‘POI’) being outside India come for a visit to India. However, considering the abuse of tax provisions, there was modification of the residency threshold to 120 days for high-income individuals. Further, there was introduction of the deemed residency provisions for IC earning income from Indian sources exceeding prescribed threshold and who are not liable to tax in any other jurisdiction were brought within the Indian tax framework This amendments strengthens the legislative intent to address tax avoidance by individuals who strategically manage their period of stay to remain outside the ambit of tax residency in India despite having substantial economic interests or connections with India. Below is the flow chart capturing the determination of residential status of an individual:

b. Scope of Income Taxation (Sec 5 of ITA)

Once the residential status is determined, the scope of income taxable in India depends on such classification:

| Particulars | Residents/ ROR | NOR | NR |

| Income accrued or deemed to accrued in India | Yes | Yes | Yes |

| Income received or deemed to be received in India | Yes | Yes | Yes |

| Income accrued or arising outside India | Yes | Yes (only when it is derived from a business controlled in or a profession set up in India) | No |

c. Source-Based Taxation (Sec 9 of ITA)

In addition to residence-based taxation, Indian law also follows source-based taxation principles. Sec 9 of ITA extends the scope of income by deeming certain incomes to accrue or arise in India if they have a sufficient nexus with India, such as income arising through a business connection in India, property or assets located in India, services rendered in India, or income by way of interest, royalty, or fees for technical services payable by specified persons. This provision operates as a source-based taxation, ensuring that income economically linked to India is subject to tax in India.

d. Interplay of tax residency and income taxation

- The interaction of Sec 5 and 9 determines the overall tax liability:

- RORs are taxed on global income

- NRs are taxed only on India-sourced income

- NORs are taxed on:

- Indian income; and

- Foreign income linked to business/profession in India

- Further, pursuant to the introduction of the 120-day residency rule and the deemed residency provisions, certain individuals who were previously treated as NR may now be reclassified as ROR. Owing to this change in residential status there can be some neutral consequences (illustratively, no change in reporting requirements under ITR forms for an individual or exemption of interest earned on NRE account). However, as taxability under the ITA is linked to the residential status of the taxpayer, such reclassification may have some significant implications. The illustrative list is of consequences triggered are enumerated below:

- Where India sourced incomes like dividends, interest, etc are smaller in quantum, being NOR, offers advantage of lower slabs for such incomes instead of gross basis taxation.

- NOR is entitled to rebate under sec 156 of ITA 2025 (corresponding to sec 87A of ITA 1961) and can also avail specified deductions available only to residents under Chp VIII of ITA 2025 (corresponding to Chp VI-A of ITA 1961).

- Benefit of presumptive tax under Sec 58 (corresponding to sec 44AD of ITA 1961) to resident individual engaged in eligible business and having prescibed turnover or gross receipts may be availed by NOR. Similarly, Sec 58 (corresponding to sec 44ADA of ITA 1961) may apply to NOR individual engaged in profession having prescribed gross receipts.

- Further, there can be consequences in hands of counter party dealing with individuals becoming NOR, illustratively:

- Deemed gift taxation under sec 9(8) of ITA 2025 (corresponding to 9(1)(viii) of ITA 1961): Sum paid as per Sec 92(2)(m)(i) of ITA 2025 (corresponding to of Sec 56(2)(x)(a) of ITA 1961) without consideration by resident to NR or foreign company and which arises outside India is taxable in hands of NR. Accordingly, such a receipt may be subject to tax in India if the deemed accrual provisions apply.

- While deducting TDS, the payer will have to apply provisions as applicable to payments to residents (such as Sec 393(1) & (3) of ITA 2025 corresponding to Sec 194A, 194C, etc. of ITA 1961), instead of Sec 393(2) of ITA 2025 (corresponding to Sec 195 of ITA 1961) which applies to non-residents.

- Liberal provisions of sec 35(b)(i) of ITA 2025(corresponding to sec 40(a)(ia) of ITA 1961) may apply to deductor where disallowance is restricted to 30% of the expenditure and not 100%.

Global perspective and Emergence of Dual Residency:

- While the above discussion explains the Indian domestic framework, it is equally important to understand how cross-border taxation operates globally, as dual residency is largely a product of interacting domestic tax systems:

- Globally, taxing rights are broadly based on two principles

- residence-based taxation

- source-based taxation.

- Under the residence principle, a country taxes the worldwide income of persons who qualify as its residents, irrespective of where such income is earned. Under the source principle, a country taxes income that arises within its territory, regardless of the taxpayer’s residence.

- In practice, most countries adopt a hybrid approach, exercising taxing rights both as a residence State and as a source State. This often results in the same income being taxed in more than one jurisdiction. The concept of worldwide income taxation being intrinsic to residence-based systems, becomes a primary driver of potential double taxation.

b. The emergence of dual residency is a direct consequence of the divergent criteria used by different jurisdictions to determine tax residency. Many countries adopt a physical presence test or incorporation test, while many rely on factors such as citizenship, domicile or place of effective management. These overlaps have become more pronounced in India following the introduction of deemed residency provisions, which expand the scope of individuals qualifying as residents under domestic law. This dual residency can arise in several practical situations, some of which are illustrated below:

- Cross-border Employees:

Individuals deputed to another jurisdiction may meet residency thresholds in the host country while continuing to qualify as residents in their home country under its domestic law.

- Frequent Travellers / Business Executives:

A frequent traveller may be considered resident in India by virtue of deemed residency provisions, while concurrently qualifying as a resident in another jurisdiction based on its domestic tests. - Returning Individuals / Transitional Years:

Individuals returning to India after overseas employment often face overlapping residency in the year of transition, as residency tests in India (based on the tax year) may not align with foreign jurisdictions (often calendar year based). - Returning Individuals / Transitional Years:

Individuals returning to India after overseas employment often face overlapping residency in the year of transition, as residency tests in India (based on the tax year) may not align with foreign jurisdictions (often calendar year based). - Dual Residency of Companies:

A company may also be treated as a resident in two jurisdictions owing to differing domestic tests. For instance, a company incorporated in State A may be regarded as a resident of that country by virtue of incorporation, while State B may treat it as a resident based on the location of its place of effective management (POEM).

Conflict Resolution in Dual Residency: A DTAA Perspective

- Given the prevalence of dual residency scenarios discussed above, it becomes essential to examine how such conflicts are resolved under tax treaties. The applicable Double Taxation Avoidance Agreement (DTAA) plays a critical role in resolving such conflicts and preventing double taxation. Sec 159 of ITA 2025 (corresponding to Sec 90 of ITA 1961) provides the statutory basis for applying treaty provisions which are more beneficial than domestic law. The sequence is well established. First, each country determines residence under their domestic law. Thereafter, the DTAA tie-breaker rules are applied to assign a single residence for treaty purposes. These tie-breaker rules do not alter domestic residence per se, but assign a single “treaty residence” for purposes of applying the distributive rules of taxation under the treaty framework.

- For individuals, the OECD Model Tax Convention (OECD Model) tie-breaker follows a structured hierarchy. Article 4(2) provides that in the case of a dual resident, the treaty residency would be determined as follows:

- Permanent home test:

The jurisdiction in which the taxpayer has a permanent home available to him. There are no rules in Indian tax laws or the treaty which define a Permanent home, hence based on commentaries and judicial analysis the following rules have emerged:

- Any form of home, may be self owned or a rented premises

- Available continuously and not occasionally

- The term ‘to have available’ in the sense of ‘possessing’, covers both the right which the master of a house has and the right of its owner or tenant to determine occupancy of the dwelling

- Length of the individual stay is of no or of only little importance

- Generally, a hotel may not be considered a permanent home, if the facts suggest that accommodation would always be available to the taxpayer as a matter of right, it may be considered a permanent home.

- Even if a person owns a particular residential property in a particular jurisdiction, it may not be considered a permanent home if the taxpayer has given the said property on rent and the taxpayer does not have the right to use the property at any given time

ii. Centre of vital interests:

If he has a permanent home in both jurisdictions, the jurisdiction with which his personal and economic relations are closer. Personal interests would include: his family and social relations; his activities (e.g. political, cultural etc.); Schooling of children; etc. Economic interests would include: his place of business, his occupation, his income and property, assets owned, the place from which he administers his property, etc.

If personal relations are closer with one contracting state while the economic relations are closer with the other, the decisive point is which of the two localities is of greater significance to the taxpayer. Wherever the two criteria are of equal weight, the OECD commentary recommends that the personal acts must receive special attention.

iii. Habitual abode test:

Where the Centre of vital interests cannot be determined, or where the individual does not have a permanent home in either jurisdiction, residence is allocated to the State in which the individual has a “habitual abode.” In simple terms, this refers to the country where the individual stays more regularly or frequently. The analysis is not limited to a particular type of stay—rather, it considers the overall pattern of physical presence in each State. All periods of stay are relevant, whether at a permanent home or elsewhere, and regardless of the purpose (such as employment, travel, or personal reasons). The focus is therefore on determining in which jurisdiction the individual’s presence is more consistent and recurrent over time.

iv. Nationality test:

If the individual has a habitual abode in both or neither jurisdiction, the individual will be treated as resident of the jurisdiction of which he is a national.

v. Mutual Agreement Procedure (MAP):

If the individual is a national of both or neither jurisdiction, then he shall be resident of jurisdiction, as mutually agreed by the competent authorities of both jurisdictions. However, certain treaties, like India-Japan DTAA, depart from this sequential approach and mandate competent authority determination at the outset, thereby introducing uncertainty and potential delays in finalizing treaty residence.

c. Generally, in the case of non-individuals, particularly companies, the tie-breaker rule typically rests on the place of effective management. Thus, a company that is incorporated in one State but effectively managed from another may, for treaty purposes, be regarded as resident in the latter. However, some treaties specifically require resolution through mutual agreement between competent authority agreement. On the other hand, some treaties are differently worded and at times take the dual resident companies out of the scope of DTAA, like India US DTAA explicitly provided that a dual resident company would be considered outside the scope of the relevant DTAA thereby limiting the access to DTAA by such companies.

d. The State to which treaty residence is allocated is often referred to as the “Winner State”, while the other assumes the role of the “Loser State”. This distinction is significant, as the Winner State retains residence-based taxation rights, whereas the Loser State is constrained to exercise only such taxing rights as are allocated under the DTAA, usually in a source-based capacity. The jurisdiction, being the treaty residence State, is obliged to provide relief for taxes paid in other jursdictions, typically through a foreign tax credit mechanism. However, it will be pertinent to note that in order to avail the treaty benefits of winner state, it will be important to seek a Tax Residency Certificate (TRC) of the winner state by the individual.

e. The practical tax consequences flow directly from this allocation. Further, it is to be noted that only for the limited purpose of treaty application, the individual may be considered as NR in India. For domestic purposes, the individual will be considered as NOR and other implications as discussed above in residency and income interplay will continue to apply.

Absence of DTAA: Tax Implications of Unresolved Dual Residency

- While DTAAs provide a structured mechanism to resolve dual residency conflicts, the position becomes significantly more complex in their absence. Where no DTAA exists between the two jurisdictions, or where the applicable treaty fails to resolve dual residence (including situations where certain dual residents are expressly excluded from its scope), there is no mechanism available to resolve the conflict and prevent double taxation. In such cases, both countries may assert full residence-based taxation under their domestic laws, leading to unrelieved double taxation. India, in such scenarios, would tax the individual or entity on global income if they qualify as resident under domestic law, without treaty-imposed limitations.

- Foreign Tax Credit (FTC), i.e., credit for taxes paid in another jurisdiction, is not automatically available; it is granted only when permitted under domestic law or an applicable treaty. In the Indian context, Sec 159 of ITA 2025 (corresponding to Sec 90 of ITA 1961) primarily governs relief under tax treaties, and the mechanics of credit are typically embedded in the “Elimination of Double Taxation” article of the relevant treaty. Accordingly, where no DTAA has been entered into with the other resident State, the statutory route under above quoted sections of ITA is unavailable for that bilateral relationship, and there is no treaty obligation compelling India to recognise or credit taxes paid abroad on a residence basis.

- This position is also consistent with the OECD Model Convention and its Commentary on Article 4. The concept of “residence” for treaty purposes, along with the tie‑breaker rules and the method article for granting relief, operate only within the confines of a DTAA. In the absence of such an agreement, there is no mechanism to allocate a single treaty residence and, more importantly, no reciprocal commitment between States to relieve double taxation through a credit or exemption method.

- Sec 160 of ITA 2025 (corresponding to Sec 91 of ITA 1961) provides for unilateral relief in certain cases where no DTAA exists. However, its scope is limited and does not effectively address cases where both jurisdictions tax global income based on residence. In such cases, both countries may tax the same global income based on residence. Further, the Indian law does not contain any provisions to resolve such dual residency conflicts or to mandate FTC in respect of taxes levied by another State on a competing claim of residence. Thus, the absence of a legal obligation on India to grant FTC for taxes paid to the other resident State in a no‑DTAA setting creates a scenario of double taxation without any relief.

Issues under dual residency case

Even where a DTAA exists, practical challenges arise in applying residency and treaty provisions, particularly in cases involving timing mismatches, subjective interpretation of tie-breaker rules and documentation:

- Different tax period for different countries:

- India determines residential status based on its Tax year (TY) i.e. from April 1 to March 31, whereas many foreign jurisdictions use the calendar year (CY) i.e. January 1 to December 31. Since treaty residence is determined for a specified period, misalignment in tax years may result in partial application of treaty benefits, requiring careful allocation of income across periods. This can be illustrated through the following examples:

Illustration 1: An IC may qualify as a NOR in India for a particular TY (e.g., TY 2025-26) but simultaneously be considered a resident in a foreign country (State X) for the overlapping calendar year (CY 2025 & CY 2026). If the treaty’s tie-breaker rules allocate residence to State X, for treaty purposes, India may treat the individual as a non-resident for the relevant tax year and apply treaty-limited withholding tax on India-source income, subject to availability of required documentation like TRC. However, India will continue to treat the individual as a resident (i.e. NOR) under domestic law.

Illustration 2: Consider a person who is NOR in India for the TY 2025–26. At the same time, as per the domestic law of a foreign state, the person is a resident for CY 2025 but NR for CY 2026. Since the Indian TY 2025–26 overlaps with CY 2025 for part of the year, dual residency arises during this overlapping period and must be resolved using the treaty’s tie-breaker provisions. The remainder of the TY is aligned with CY 2026, where the person is NR in the foreign country, there is no dual residency. This situation does not result in a split residency case, but rather a period of dual residency limited to the overlapping timeframe, complicating the application of treaty provisions.

ii. This temporal mismatch complicates residency assessments and treaty benefit claims, requiring careful analysis of overlapping periods and appropriate application of tie-breaker rules to avoid double taxation or denial of treaty benefits.

b. Application challenges of tie-breaker tests:

- Fact Sensitive exercise: The language of Article 4(2) is clear regarding the order to be followed while determining the treaty residency in the case of dual residents. It is important to note that some of the conditions are subjective in nature and are used to determine which jurisdiction has a closer tie to the taxpayer. Therefore, this being a fact sensitive exercise, one needs to consider all the facts holistically and carefully while applying the various tie-breaker tests.

- Determining the Centre of Vital Interests Amid Dual Permanent Homes: The requirement to ascertain with which State an individual’s personal and economic relations are closer involves subjective judgment. Assessing factors like family ties, occupation, and property administration can be complex, especially when ties are balanced or conflicting. For example, an individual may have family in one State but conduct business primarily in another, making it difficult to pinpoint the true centre of vital interests.

- Weight of Personal Acts Versus Objective Facts: The OECD commentary emphasizes giving special attention to personal acts, but it can be challenging to weigh these against objective facts such as property ownership or duration of stay. For instance, if an individual keeps their original home in one State where their family and belongings are, but also sets up a new home in another State where they spend some time, it can be difficult to decide which home truly represents their main personal and economic ties. The question arises whether the emotional connection to the original home or the actual time spent living in the new home should carry more weight in determining their centre of vital interests.

- Ambiguity in Defining “Habitual Abode”: The concept of habitual abode is not strictly defined by the number of days spent but by frequency, duration, and regularity of stays forming a settled routine. This introduces interpretational uncertainty, as what constitutes a “settled routine” may vary widely between cases. For example, frequent short stays in two States might qualify as habitual abode in both, complicating residence determination. Further, for individuals without a permanent home in either State (e.g., those living in hotels or transient accommodations), assessing habitual abode based solely on stays without considering reasons for presence can be factually difficult.

- Dual Habitual Abode and Nationality as Secondary Criteria: When habitual abode exists in both or neither State, nationality becomes the next criterion. However, dual nationality or lack of nationality in either State creates interpretational challenges and may lead to reliance on MAP, which can be time-consuming and uncertain.

- Complexity in Cases of Frequent Travel and Multiple Residences: Individuals with multiple residences and frequent travel between States pose factual difficulties in tracking and verifying patterns of presence. This complexity can hinder clear application of the tie-breaker rules and increase disputes between taxpayers and tax authorities.

- Risk of Conflicting Outcomes: When each Contracting State independently applies residency or tie-breaker tests, potentially reaching different conclusions about an individual’s or entity’s tax residence. Such discrepancies can result in double taxation or denial of treaty benefits, creating uncertainty and disputes. Resolving these conflicts often necessitates escalation through the MAP under the relevant tax treaty to achieve a coordinated and fair outcome.

c. Documentation and Key Issues in Availing Treaty Benefits Post Tiger Global Ruling[1]:

- Essential Documentation for Treaty Benefit Claims: Sec 159 of ITA 2025 (corresponding to Sec 90 of ITA 1961) mandates availing a valid Tax Residency Certificate (TRC) in order to claim the treaty benefit. Further, the dual resident may also be required to furnish the following documents along with TRC to an Indian Resident payer of income in order to avail treaty benefits:

- Form 41 (corresponding to Form 10F of ITA 1961) (if applicable);

- A no-Permanent Establishment (PE) declaration; and

- A beneficial ownership (BO) declaration.

- Position and Role of Tax Residency Certificate (TRC): The Supreme Court’s Tiger Global ruling1 clarified that TRC remains a mandatory eligibility document under Indian law for claiming treaty benefits but serves only as prima facie evidence of residence, not conclusive proof. Tax authorities may look beyond the TRC to test substance over form, evaluating whether there is genuine liability to tax in the claimed residence jurisdiction. This includes examining where effective management and key decisions occur, consistent with Article 4 of the relevant treaties. Mere possession of a TRC cannot alone compel treaty relief if facts suggest control outside the treaty country or potential tax avoidance.

- Substance and Evidence Requirements: Due to intensified scrutiny following Tiger Global ruling (supra), taxpayers should be prepared to provide detailed substance documentation to support their treaty residence claims. This may include evidence such as expenditure records, directors’ travel logs, remuneration details, and email correspondence. Authorities may reject treaty residence claims in the absence of such objective evidence demonstrating effective management and genuine tax liability in the treaty jurisdiction.

Practical Case Studies:

The practical implications of dual residency can vary depending on the availability of DTAAs, availability of dual residence resolution clause, the outcome of tie-breaker tests, and the positions adopted by taxpayers and withholding agents. Further, the issue becomes more complex as there is limited guidance available on this aspect under the ITA or in the form of judicial precedents. In this regard, an attempt is made to evaluate the tax consequences under various scenarios in the case study format:

Common assumptions for all the case studies discussed below:

- When a person’s residence tie breaks to any state, he cannot automatically avail the treaty benefit. As per the ITA, a person claiming relief under the DTAA necessarily needs to obtain a TRC from the jurisdiction in which he claims to be a resident. Thus, in following case studies, it is assumed that the TRC has been obtained (even from loser state) and the necessary information as is specified to be provided along with the TRC is also provided to the counter party (the payer/deductor).

- It is assumed that the deductor is aware of the dual residency (possibly because they are group entities, related parties, in joint venture relationship or information on DRC status has been shared by the income recipient to the deductor).

- Person is resident of 2 foreign countries, India is the source country and India has DTAAs with both the countries:

- Case Facts: The entity, say XYZ, is tax resident of State A as also State B in terms of respective domestic law of State A and State B. XYZ sources income from India, which is chargeable to tax in India under the ITA. India has DTAAs with States A and B. India-A DTAA provides for a 10% withholding on specified income, whereas India-B DTAA provides for a 15% withholding.

- Issue: Can the benefit of 10% rate under the India-A DTAA be availed?

- Scenario 1: No resolution of Dual residency:

- In this case, there is either no DTAA between State A and State B or the DTAA between A and B fails to resolve residency issue of the entity. Accordingly, the entity continues to be resident of State A as also State B.

- Beneficial of the two DTAAs needs to be considered because from an India perspective, XYZ is not a resident of India under both the DTAAs [India A DTAA and India B DTAA]. Instead, XYZ qualifies as a resident of “the other Contracting State” in case of both of the DTAAs. Accordingly, when two provisions (from two DTAAs) equally apply, the one that is beneficial for the taxpayer (in this case, income-recipient, XYZ) should be applied.

- Further, the OECD guidance[2] suggests that when an income qualifies for benefits under two tax treaties, the source state may comply by applying the lower of the two applicable tax rates. In this context, since the India‑B DTAA permits withholding tax up to 15% and the India‑A DTAA restricts it to 10%, applying a 10% withholding rate satisfies both treaties. Charging tax at 10% does not conflict with the India‑B DTAA, as it is within its maximum limit, whereas applying a higher rate would breach the India‑A DTAA and go against a good‑faith interpretation of treaty obligations.

- However, this position is not explicitly provided under Indian law and may be subject to litigation risk. Thus, a more conservative approach may involve withholding tax at domestic rate depending upon the nature of income (which may be higher than the DTAA rates) and the recipient can claim the excess tax as refund by filing income tax returns.

- Scenario 2: XYZ tie breaks to State B:

- As the XYZ is not expected to be comprehensively taxed in the other jurisdiction (i.e. State A), the Indian deductor may adopt a conservative approach and disregard the India‑A DTAA at the withholding stage. Instead, reliance may be placed on the India‑B DTAA, and tax may be withheld at 15%, being the rate prescribed therein.

- From the recipient’s perspective, however, it may still take a position that it is entitled to the benefit of the more favourable India‑A DTAA, which limits taxation in India to 10%. While such benefit may not have been applied at the withholding stage by deductor, the recipient may seek to assert its treaty eligibility at the time of filing its tax return in India and accordingly claim a refund of any excess tax withheld (i.e. above 10%), on the basis that treaty entitlement may be examined and granted during assessment proceedings. However, this may be viewed as aggressive and could be considered risky, with a low likelihood of holding up if challenged.

- Scenario 3: XYZ tie breaks to State A:

- Since XYZ tie-breaks as a resident of State A, XYZ may be considered as comprehensively taxed in State A. Indian deductor may apply the India-A DTAA and deduct tax @10%. Accordingly, there should be no apparent conflict from an Indian deductor’s perspective.

- Where the tax deductor desires to act more conservatively and apply the higher withholding tax rate, the recipient may be advised to file a tax return in India and claim refund of the excess taxes withheld.

b. Person is resident of 2 foreign countries, India is the source country and India has DTAAs with one of the countries:

- Case Facts: The entity, say XYZ, is tax resident of State A as also State B in terms of respective domestic law of State A and State B. XYZ sources income from India. Such income is chargeable to tax in India terms of ITA. India has DTAA with only state A, which provides for a 10% withholding.

- Issue: Can the benefit of 10% rate under the India-A DTAA be availed?

- Scenario 1: No resolution of Dual residency:

- Unlike the previous scenario where competing treaty benefits existed, as there is no DTAA with state B, Accordingly India-A DTAA may be applied, as the entity qualifies as a resident of State A under the applicable DTAA and taxes may be deducted by the payer at the DTAA prescribed rate of 10%. Accordingly, there may be no conflicting situation arising to XYZ.

- However, considering a more conservative approach taxes may be withheld at domestic tax rates (which may be higher that the DTAA rates) and XYZ may be advised to claim refund of excess tax deducted over 10%.

- Scenario 2: XYZ tie breaks to State A (DTAA with winner state):

- As the recipient is comprehensively taxed in State A which is the winner state, the Indian deductor & XYZ may have comfort in applying the DTAA which India has with State A while deducting taxes and filing return of income respectively.

- Scenario 3: XYZ tie breaks to State B (DTAA with loser state):

- As the recipient is not likely to be comprehensively taxed in the loser state (i.e. State A), the Indian deductor may be advised to act conservatively and not consider India’s DTAA with the loser state (i.e. A). As there is no DTAA with State B and DTAA with State A is unlikely to be applicable, the deductor may withhold taxes as per Indian domestic tax law.

- From a recipient’s perspective, it can consider claiming the benefit of DTAA with State A to claim refund of tax in excess of the distributive right provided in DTAA with State A by raising claim to DTAA entitlement in its tax return. However, this may be viewed as aggressive and could be considered risky, with a low likelihood of holding up if challenged.

c. Dual resident with India being one of the resident country:

- Case Facts: The entity, say XYZ, is tax resident of India as also State B in terms of respective domestic law of India and State B. XYZ sources income from State C, thereby State C will be source jurisdiction.

- Issue: Which DTAA should be applied?

- Scenario 1: No resolution of Dual residency:

- In this scenario either the DTAA between India and B fails to resolve residency issue of the entity or there is no DTAA between India and State B. Accordingly, the entity continues to be resident of India as also State B.

- In this scenario, taxation rights of India in relation to the XYZ are not restricted by India-B DTAA Accordingly, the XYZ ought to be regarded as a resident of India and comprehensively liable to tax in India for the purpose of India’s DTAAs with third countries.

- Hence the entity should be able to access to India’s DTAAs with third countries. The entity may be subject to global income tax liability, both in India and in State B since it is likely to also be comprehensively taxed in State B. The entity may have challenges in claiming foreign tax credit in India for taxes that may be levied in State B on the basis that it is also a resident of State B.

- Taxation in respect of income source from State C will depend on the view which the State C will take about entitlement of the entity to DTAA benefit. Since the entity does not lose its residency in India, the State C may grant benefit of DTAA between India and State C. Accordingly, taxes that are so paid in terms of DTAA of India with State C should qualify for foreign tax credit in India in terms of India-C DTAA.

- Scenario 2: where dual residency is resolved with India emerging as the Winner State:

- To resolve a dual residency situation, a DTAA must be in place to provide the tie-breaker rules. Therefore, this cannot be a case where no DTAA exists between India and State B.

- Accordingly, under the DTAA between India and State B, XYZ is regarded as having its place of effective management in India. As a result, the dual residency is resolved in favour of India.

- As XYZ will be comprehensively liable to tax in India, the XYZ will able to access India’s DTAA with third countries. Taxation in State B will be in terms of DTAA between India and State B. India will be expected to grant tax credit in respect of taxes paid in State B in terms of India and State B DTAA.

- Taxation in respect of income source from State C will depend on the view which the State C will take about entitlement of the entity to DTAA benefit. Since India is a winner State, the State C is expected to grant benefit of DTAA between India and the State C. Taxes which are paid in terms of DTAA of India with State C should also qualify for tax credit in India in terms of India-C DTAA.

- Scenario 3: where dual residency is resolved with India emerging as the Loser State:

- 1. To resolve a dual residency situation, a DTAA must be in place to provide the tie-breaker rules. Therefore, this cannot be a case where no DTAA exists between India and State B.

- Accordingly, under the DTAA between India and State B, XYZ is regarded as having its place of effective management in State B. As a result, the dual residency is resolved in favour of State B.

- XYZ will be comprehensively liable to tax in State B. Access to India’s DTAAs with third countries would depend on whether the entity continues to qualify as a resident of India for treaty purposes. In this case, XYZ may claim the treaty benefit under the State B-State C DTAA.

- As this position may also be subject to interpretational challenges and differing views by tax authorities, XYZ may put forth a claim for availability of India-State C DTAA benefit in the State C. The availability of the DTAA benefit would largely depend on how State C applies the provision. From India tax authorities’ perspective, they should be neutral to this proposition since, in any case, in respect of income sourced in State C, the right to tax such income would generally be with the winner State (i.e. State B) of the tie-breaker between India and State B.

Conclusion:

In an increasingly interconnected world, dual residency has emerged as a complex and often unavoidable reality for globally mobile individuals and businesses. While domestic tax provisions and DTAAs provide a structured framework for allocating taxing rights, their practical application frequently involves nuanced factual analysis and interpretational challenges. This complexity is further compounded by the limited judicial guidance available under Indian jurisprudence, particularly on the application of treaty tie-breaker rules and dual residency scenarios. Accordingly, a careful evaluation of residency rules, treaty provisions, and documentation requirements is essential to mitigate the risk of double taxation. A proactive and well-informed approach will therefore be critical for taxpayers navigating the evolving landscape of cross-border taxation.

[1] Tiger Global International Holdings – Civil Appeal No. 262 of 2026

[2] paragraph 74 of the 1999 OECD Report on “The Application of the OECD Model Tax Convention to Partnerships”. This report was adopted by the Committee on Fiscal Affairs, was made available to the public on 20 January 1999.

[The author can be reached at poojamaru31@gmail.com.]