Peer Review Decoded: What Every CA Firm Must Know Today

| Imagine investing years building your CA firm’s reputation — only to be disqualified from a coveted statutory audit engagement because your firm lacks a valid Peer Review certificate. This is no longer a hypothetical scenario. With mandatory Peer Review now covering most mid-sized and large firms, the question is not whether your firm will face a review — but whether it is ready. |

A Practising CA Firm’s Perspective

Introduction: The Genesis and Evolution of Peer Review

Over the past decade, Peer Review has transitioned from a voluntary quality initiative to a mandatory requirement for CA firms engaged in assurance services. Regulatory expectations from bodies such as NFRA, SEBI, RBI, Banks and the Comptroller & Auditor General (C&AG) have reinforced the importance of Peer Review as a benchmark of audit quality and professional discipline.

For CA firms of all sizes engaged in assurance services, Peer Review has ceased to be a distant regulatory requirement and is fast becoming a pre-condition for growth, credibility, and sustainability. What was once perceived as a compliance requirement is now a defining factor in professional excellence.

Objective of Peer Review: Beyond Mere Compliance

The main objective of Peer Review is to ensure that, while performing assurance services, firms:

- Comply with applicable technical, professional, ethical, and legal standards; and

- Maintain robust systems, processes, and clear documentation to support quality outcomes.

Importantly, Peer Review is not about identifying errors or questioning professional judgement. Rather, it evaluates whether the firm has adequate systems in place to consistently deliver high-quality work.

In essence, Peer Review answers one key question:

“Does the firm have the right processes to ensure quality?”

Scope of Peer Review: More Than Just Audit Files

A common misconception is that Peer Review is limited to reviewing selected audit files. In reality, its scope is considerably broader — extending to a comprehensive evaluation of the firm’s overall functioning and quality framework.

Peer Review evaluates:

- Compliance with Standards on Auditing, Accounting Standards, and Code of Ethics

- Quality control framework and internal policies

- Documentation practices and reporting quality

- Independence and ethical compliance

- Training and competency of staff

- Overall internal control environment of the firm

Peer Review is best understood as a holistic assessment of the firm’s operational and quality management systems — not merely a review of selected audit files. This broader lens ensures that the firm consistently delivers high-quality professional services and maintains documentation to the expected standards.

In essence, Peer Review evaluates the firm as a whole — not merely its engagements.

What is the Peer Review Period?

Peer Review typically covers the three financial years immediately preceding the year of review, unless otherwise specified by the Peer Review Board.

Applicability of Peer Review: Who Needs It?

Based on ICAI’s phased implementation (effective April 1, 2022, and subsequent updates):

Peer Review is mandatory for firms undertaking statutory audits of:

- Listed entities

- Large unlisted public companies having:

- Paid-up capital exceeding ₹500 crore; or

- Annual turnover exceeding ₹1,000 crore; or

- Outstanding loans, debentures, and deposits exceeding ₹500 crore in aggregate

- Entities raising funds from the public, banks, or financial institutions, exceeding ₹50 crore

- Any body corporate, including trusts, covered under the definition of Public Interest Entities (PIEs)

- Central statutory audit of Public Sector Banks

- Firms having 4 or more partners

Deferred Applicability — Phase IV (up to December 31, 2026):

- Statutory branch audits of Public Sector Banks

- Firms having 3 or more partners

Additionally:

- Firms may opt for voluntary Peer Review

- The Board may initiate a special Peer Review in specific cases

- New Units (firms with limited or no assurance engagements) are also eligible

In practice, most mid-sized and large CA firms already fall within the mandatory ambit.

What are Assurance Services?

An Assurance Engagement is one in which a practitioner expresses a conclusion designed to enhance the degree of confidence of intended users — other than the responsible party — regarding the evaluation or measurement of a subject matter against specified criteria.

In simple terms, Assurance Services involve independent verification and reporting to provide credibility and reliability to information.

| Assurance Engagements ✔ (Peer Review Applicable) | Non-Assurance Services ✘ (Peer Review Not Applicable) |

| • Statutory Audit • Tax Audit • GST Audit • Internal Audit • Concurrent Audit • Certification work (Form 15CB, Net-worth, turnover, etc.) | • Management consultancy engagements • Representation before various Authorities • Preparing tax returns or advising clients in taxation matters • Compilation of financial statements • Engagements solely to assist the client in preparing, compiling or collating information other than financial statements • Providing expert opinion solely on the basis of facts provided by the client • Due diligence engagements |

Understanding this distinction is critical, as Peer Review applies to all Assurance Engagements.

Key Areas Evaluated During Peer Review: Beyond Just Audit Files

- Quality Control Systems

- Policies aligned with SQC 1 and applicable Quality Management Standards

- Monitoring and review mechanisms

- Compliance & Ethics

- Independence declarations

- Conflict of interest checks

- Adherence to ICAI Code of Ethics

- Engagement Execution

- Planning, execution, and supervision of audits

- Compliance with Standards on Auditing

- Quality and completeness of documentation

- Firm Infrastructure & Capacity

- Staff training and development

- Availability of resources and systems

- Adoption of frameworks such as ICAI’s Audit Quality Maturity Model (AQMM)

- Compliance with Directions issued by the Council

- Fees charged

- Number of audits undertaken

- Unique Document Identification Number (UDIN) generation and maintenance of records

- Other prescribed records

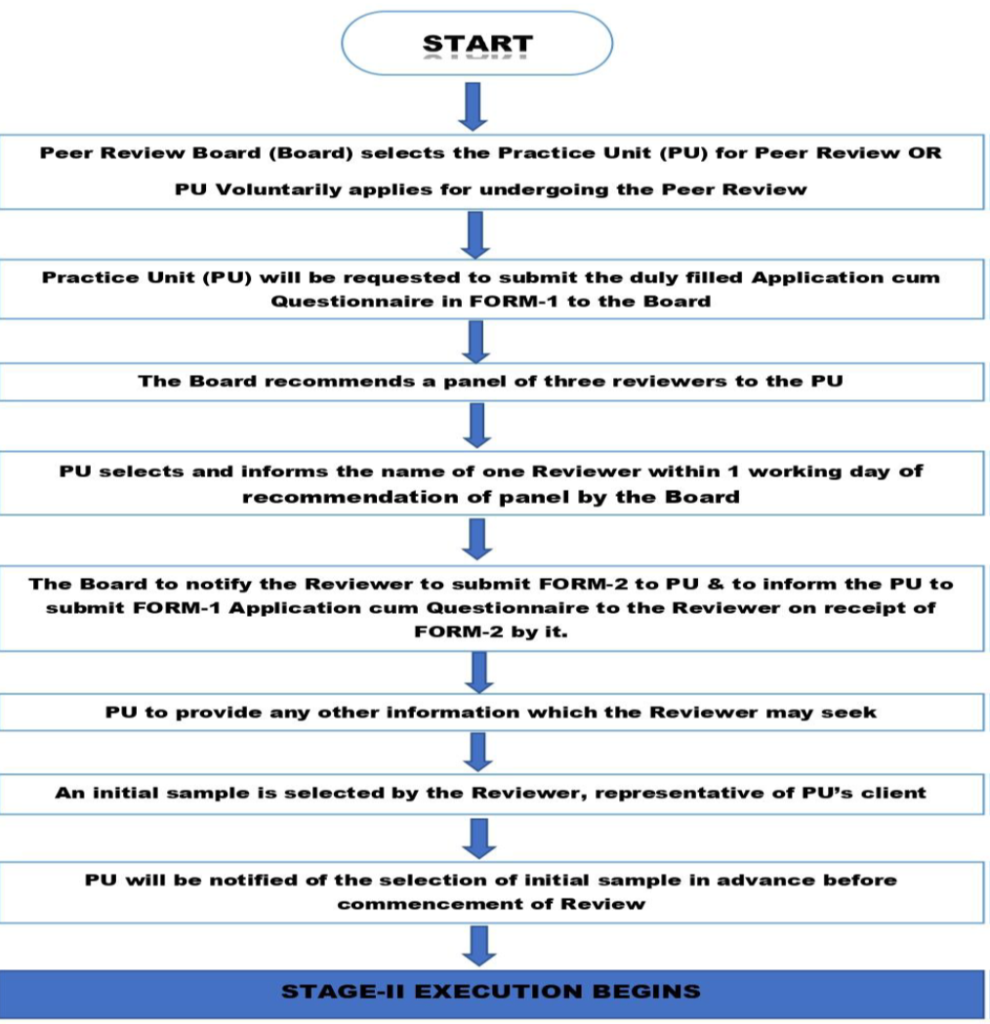

Procedure for Peer Review: How It Works

Stage I: Peer Review Initiation

Stage II: On-Site Procedure

- The Reviewer plans the on-site review in consultation with the Firm. The Reviewer shall provide the Firm with a minimum of 2 working days’ notice to prepare the necessary records.

- The visit may be conducted at the Firm’s head office and/or branch(es).

- The on-site review generally takes 2 to 6 working days; for a New Unit, it is limited to 1 working day.

- The Reviewer evaluates key general controls to assess the degree of reliance that can be placed on the Firm’s systems and processes. This includes:

- Assessment of Independence

- Maintenance of Professional Skills and Standards

- Outside consultation practices

- Staff recruitment and development mechanisms

- Overall office administration practices

- Along with the above controls, selected sample engagement files are also reviewed by the Reviewer.

- Upon completion of the on-site review, the Reviewer submits a Report to the Peer Review Board based on observations made during the review.

Stage III: Reporting by the Peer Reviewer

Upon completion of the on-site review, where the Reviewer is satisfied, an Unqualified Peer Review Report is submitted to the Peer Review Board.

In cases where deficiencies or non-compliances are observed, the Reviewer communicates findings to the CA Firm through a Preliminary Report, seeking clarification or representations. Based on the response received, if the Reviewer remains unsatisfied, a Qualified Report is submitted to the Board, clearly stating the reasons for qualification. If the Reviewer is satisfied with the response, an Unqualified Report is issued.

Review of Report by Peer Review Secretariat and Issuance of Peer Review Certificate

After submission of the Peer Review Report, the Peer Review Secretariat undertakes a detailed administrative review to ensure that the report is complete in all respects and is accompanied by all prescribed documents. The report, along with supporting documentation, is then placed before the Board for consideration.

In cases where the report is qualified, the matter is examined by the Board, which may decide to conduct a Follow-On Review after a stipulated period, generally one year from the date of the Report, which may be reduced to a minimum of six months. The firm is informed of the reasons why the certificate cannot be issued and the timeline for the Follow-On Review.

Where an unqualified report is issued, the Board issues the Peer Review Certificate. The Certificate specifies the validity period, which is generally three years.

Readiness of the CA Firm: Key Documents and Records

To ensure a smooth and efficient Peer Review process, the Practice Unit should keep the following documents, records, and information organised and readily accessible before the review begins:

| Category | Documents / Records Required |

| Basic Documentation | • Application cum Questionnaire (Form 1) • Engagement list for the review period • Details of partners, staff, and organisational structure • Copy of the latest certificate issued by ICAI regarding the constitution of the firm |

| Policies & Manuals | • Quality Control Policies and procedures (including SQC 1 aligned documentation) • Human Resource (HR) Policy Manual • Office Manual / Standard Operating Procedures (SOPs), if any |

| Client & Engagement Records | • List of major clients and nature of services provided • Assurance Engagement files (Audit, Tax Audit, GST, Certification, etc.) • Engagement letters / appointment letters • Communication with Previous Auditor • Independence declarations and conflict of interest checks • Permanent file / working file • Management representations obtained from clients • Properly maintained working papers for selected engagements • Documentation evidencing planning, execution, and conclusion of assignments • Query Sheets, Audit Programmes, and related working papers • Review notes and sign-off records indicating ‘Prepared by’ and ‘Reviewed by’ • Checklists for compliance with applicable Standards on Auditing / Accounting Standards |

| Staff & Training Records | • Staff appointment process and appointment letters • Staff appraisal systems and documentation • Details of staff qualification and experience • Training records, attendance sheets, and development programmes conducted • Internal review / monitoring reports, if any |

| Financial & Administrative Records | • Assurance engagement register • Office infrastructure details • IT systems and data backup policies • Billing and fee records |

Keeping the above information organised and readily accessible will reduce review time, improve transparency, and ensure a more favourable evaluation outcome.

Conclusion

Peer Review is no longer a regulatory hurdle — it is a testament to a firm’s commitment to quality, credibility, and long-term sustainability. The Peer Review framework must be embraced as an opportunity for continuous improvement and professional growth. Firms that proactively embed this quality-driven mindset will enhance their credibility, strengthen stakeholder confidence, and remain well-positioned in an increasingly regulated, quality-conscious professional environment.

| “Peer Review is not a mirror that shows flaws — it is a compass that guides a firm toward professional excellence.” |