RESIDENTIAL STATUS UNDER INCOME TAX AND FEMA LAW – UNLOCKING THE CONFUSION

Taxability in India is dependent on the residential status of an individual. Residential Status is the starting point to determine

- the extent and scope of income taxable in India; and

- the extent to which a person shall be regulated for the cross border transactions.

The purpose and manner of determining residential status of a person is different under the ITA and FEMA. ITA is a revenue law and is only concerned with taxable income and the tax thereon. On the other hand, FEMA is a regulatory law and is concerned with the permissibility of the transactions undertaken by an individual depending upon his residential status.

So lets us try to unlock the confusion of the residential status as per the Income Tax Act (ITA) and the Foreign Exchange Management Act (FEMA).

RESIDENTIAL STATUS OF INDIVIDUAL AS PER INCOME TAX ACT:

As per ITA, there are three categories of residential status:-

- Resident and Ordinary Resident (ROR)

- Resident and Not Ordinary Resident (RNOR)

- Non Resident Indian (NRI)

RESIDENT AND ORDINARY RESIDENT (ROR)S.6(1):-

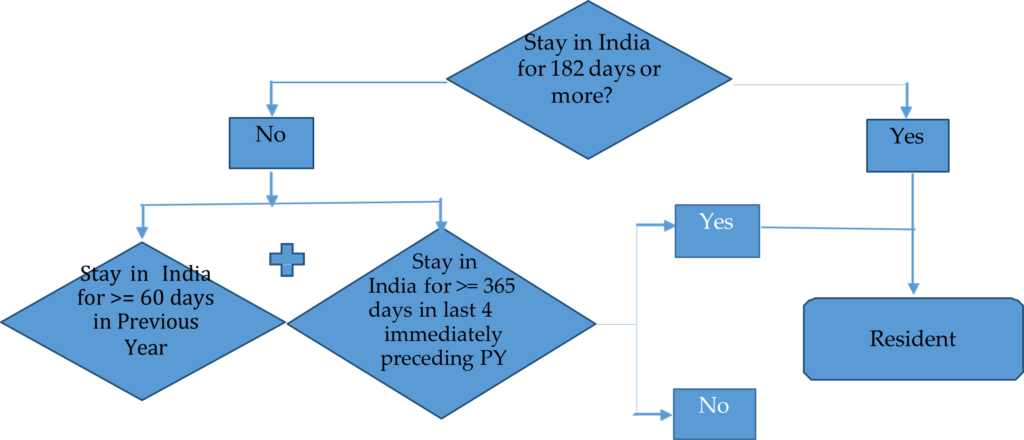

Section 6 of the ITA defines Residence. It is the number of days which determines the residential status. A person will be considered as a Resident of India if he satisfies any of the 2 conditions understated:-

| Condition | Status | |

| 1. | He stays in India for 182 days or more in a year (S. 6(1)(a)) | Resident |

| 2. | He stays in India for 60 days or more in a previous year AND stays for 365 days or more in the preceding four years ( S. 6( 1)( c)) ( Cumulative conditions) | Resident (subject to exceptions mentioned below) Many tend to forget to apply this second test for determining the residential status of the person |

Exceptions:-

- Relief has been provided in Explanation 1(a) to S. 6(1) for an Indian citizen who is resident in India and he leaves India for the purpose of employment outside India / as a member of ship crew. In such case, 60 days in 2nd condition has been substituted by 182 days. Hence, an Indian citizen who leaves India for employment in a year and has stayed in India for less than 182 days shall be considered as Non- Resident. The condition of 365 days in the preceding four years becomes redundant in such case.

- Similar concession has been provided in Explanation 1(b) to S. 6(1) for an Indian citizen or a Person of Indian Origin (PIO) who are outside India and comes on a visit to India.

In other words, the above categorized individuals falling in the exceptions are non-resident if they stay in India for less than 182 days i.e. they do not satisfy the 1st condition alone.

Amendment in Explanation 2 to Section 6(1) vide Finance Act, 2020:-

The Finance Act, 2020 (w.e.f. AY 2021-22) has amended the above exception to provide that the period of 60 days as mentioned in condition (2) above shall be substituted with 120 days, if an Indian citizen or POI has total income, other than income from foreign sources, exceeds Rs. 15 lakhs during the previous year.

Income from foreign sources means income which accrues or arises outside India (except income derived from a business controlled in or a profession set up in India).

The following table summarizes the exception to the basic test of residential status:

| Citizen of India / PIO | Indian Income > Rs.15L | Residing in India for 120 days or more | Amendment Applicable u/s 6(1) |

| Y | Y | Y | Y |

| Y | N | Y | N |

| Y | Y | N | N |

| N | Y | Y | N |

Derived from a business controlled in or Profession set up in India:-

Indian Income means Total Income earned in India + Income accrued or arisen outside India from business controlled in India or Profession set up in India.

Eg.:- Mr. A, and Indian citizen, is a Chartered Accountant having certificate of Practice from Chartered Accountants of India. He has his set up in India and a branch outside India. He advises mostly foreign clients and as such he is normally in his foreign branch for more than 182 days every year. He performs his backend operations from his office in India and during AY 2021-22, his stay in India is for 125 days. His income from Indian clientele is Rs.75 lakhs while his professional fees from foreign clients is Rs.2.25 crores.

Prior to the amendment, Mr. A is a non-resident and hence his income from Indian sources of Rs.75 lakhs was subject to Indian income tax. However, post the amendment in Finance Act, 2020, Mr. A shall become Resident in India since he is an Indian citizen residing in India for more than 120 days, having income from Indian sources exceeding Rs.15 lakhs. There could also be a view that his total income of Rs.3 crores is taxable in India since his profession is set up in India; he performs his backend operations from his office in India and assuming he has branch outside India just for conducting meetings with his foreign clients. So the onus would be on the assessee to establish as to from where were the operations done.

However it may be noted that one will have to check the DTAA Tie-Breaker Rule.

Computation of Indian Income of Rs. 15 Lakhs:-

There are many income which are otherwise exempt / deductible to Non-Resident but are taxable in the hands of a Resident individual like interest on rupee denominated bonds (S.10(4C)) and capital gain on transfer thereof (S. 47(viia)), interest on FCNR deposits, etc. Further by virtue of DTAA, many incomes may become exempt for a NR, while a Resident cannot claim the benefit under these DTAA provisions.

Therefore, there arises a question as to whether such nature of income which are exempt if the individual is a NR under the Act and whether the relief under DTAA is to be considered while computing the threshold of total income of Rs.15 lakhs?

In such cases, two views must be possible

- Residential status should be evaluated first, so as to compute the threshold of Rs.15 lakhs: Under this view, the first step would be to evaluate the residential status. Accordingly, exemptions available to a NR should not be considered till determination of residential status. Consequently, the computation of income should be made considering the individual to be a resident so as to evaluate the applicability of Rs.15 lakhs threshold.

- Exemption available to NR to be considered so as to compute the threshold of Rs. 15 lakhs: Under this view, exemption available to NR should be allowed by considering such individuals as NR and accordingly any such exempt income will not be considered while computing total income for evaluating applicability of Rs.15 lakhs threshold. However, if the total income still exceeds Rs. 15 lakhs, then such individual qualifies as RNOR and accordingly, the total income shall be reworked.

Introduction of new Section 6(1A) – Concept of Deemed Residency:-

The Finance Act, 2020 has further inserted new section 6(1A) which provides that an Indian citizen shall be deemed to be Resident in India if his total income, other than foreign sources, exceeds Rs. 15 lakhs during the previous year. However, such an individual shall be deemed to be an Indian resident only when he is

not liable to tax in any country or jurisdiction by reason of his domicile or residence or any other criteria of similar nature. Nevertheless, this provision will still need to be read with Article 4 of the applicable tax treaties (Double Tax Avoidance Agreement), which may give suitable relief.

Income from foreign sources shall have the same meaning as explained above.

Thus, from AY 2021-22, an Indian Citizen earning total income in excess of Rs.15 lakhs (other than from foreign sources shall be deemed to be resident in India if he is not liable to pay tax in any country.

A person shall be deemed to be of Indian origin if he, or either of his parents or any of his grandparents, was born in undivided India.

The following table summarizes the amendment:

| Citizen of India / PIO | Indian Income > Rs.15L | Liable to tax in any other country | Deemed to be Indian Resident |

| Y | Y | N | Y |

| Y | Y | Y | N |

| Y | N | N | N |

| Y | N | Y | N |

| N | Y | Y | N |

Why Amendment?

The Memorandum to the Finance Bill 2020 clarifies the rationale by stating that high networth individuals, who are Indian citizens and have been planning their affairs in such a manner so as to avoid paying taxes on income earned by them to any country by being non-residents of all the countries imposing income-tax. Thus, the intent of the Indian Government seems to be to plug this loophole to prevent Indian citizens from exploiting the residency rules of multiple jurisdictions to their advantage and to avoid tax in all countries (Tax Nomads).

These tax nomads would plan their stay in the different countries in such manner that their “number of days’ criteria required to be classified as resident is not met. The person in the above scenario intending to escape the “residential status”, so as to escape the clutches of tax norms, is what is referred to by the Memorandum to Finance Bill 2020 as a “Stateless Person”. This issue of “Stateless Income” was also raised during the discussion surrounding the foundation of the Base Erosion and Profit Shifting (BEPS) Action Plan and had emphasized to implement different measures to put an end to the phenomenon of “Stateless Income”.

Not Liable to Tax:-

The term “Not liable to tax” is not the same as “exemption from tax” or “non-payment of tax” or “not being subjected to tax”. The expression “liable to tax” does not necessarily imply that person should actually be liable to tax or should have paid tax. It is enough if the other contracting state has the right to tax such person, whether or not such right is exercised and irrespective of whether such person essentially pays any tax or not. This has been considered under various judgements including;

M.A. Rafiq, In re (1995) 213 ITR 317 (AAR)

Cyril Eugene Pereeira, In re (1999) 239 ITR 650 (AAR) Union of India Vs. AzadiBachaoAndolan, 263 ITR 706 (SC) Emirates Shipping Line Vs. ACIT, 349 ITR 493 (Delhi) ITO Vs. Birla Sunlife Management Co. Ltd., (2010) 3 taxmann.com 782 (Mum)

Thus based on the above paragraphs and the memorandum of the Finance Bill, one can reasonably conclude that the impact of the amendment should be only on such Indian citizens who are not liable to tax in any country by not qualifying the as resident of any country and not on those being subject to tax under the local laws of the Country like UAE.

RESIDENT BUT NOT ORDINARILY RESIDENT (RNOR) S. 6(6):-

This is applicable to Non-Residents who are returning to India. If you are not a ROR, you can still be RNOR. An individual is a RNOR is he satisfies any of the conditions understated:-

| Condition | Status | |

| 1. | He is a resident, as per the above provisions, for at least 9 out of 10 PYs prior to the PY under consideration | RNOR |

| 2. | His stay in India during the 7 PYs prior to the PY under consideration should not be 730 days or more | RNOR |

| 3. | If he is an Indian citizen AND not a tax resident in any other country AND Indian Total Income > Rs. 15 lakhs (S. 6(1A) as explained above) | RNOR |

| 4. | If he is an Indian Citizen or POI AND his Indian Total income > Rs.15 lakhs in the PY under consideration AND his stay in India in the PY ranges from 120 days to 181 days (Explanation 1(b) to S. 6(1) as explained above) | RNOR |

Note:- Generally, a person who is returning to India after 9 years of stay outside India (and who was NR for each of the 9 years) shall remain RNOR for a period of 2 years after returning to India.

NON-RESIDENT (NR):-

An individual who is not a Resident (ROR or RNOR) shall be a Non-Resident Indian.

TAXABILITY:-

| Particulars | Levy of Tax in India | ||

| Income received or deemed to be received in India | ROR | RNOR | NR |

| Yes | Yes | Yes | |

| Income accrued or deemed to be accrued in India | Yes | Yes | Yes |

| Income accruing outside India from a business controlled in or a profession set up in India | Yes | Yes | No |

| Income accruing outside India from a business controlled in or a profession set up outside India | Yes | No | No |

Notes:-

- Income received outside India, but subsequently remitted to India does not amount to receiving income in India. 1st receipt is important for consideration.

- While counting the period of stay, continuous stay or stay at a particular location in India is irrelevant.

- While computing the period of stay in India, both the days of entering in India and the day of leaving from India shall be counted in period of stay in India (conservative approach since there are many contrary judgements).

Impact of the amendments:- Once an individual gets qualified as RNOR pursuant to the amendments, he will have to go through the understated consequences:

- Widening of the scope of total income: Income accruing or arising outside India from a business in or profession set up in India shall now become taxable in the hands of RNOR.

- Benefits of exemptions lost: Various benefits available to NR will be lost on becoming RNOR.

- Benefits of presumptive scheme / concessional rate of tax lost: Various nature of income that are taxable under concessional tax rates or are exempt in the hands of NR will now be taxable at normal slab rates in the hands of RNOR.

- Uncertainty in the rate of deduction of tax at source: Since the provision of residency test is based on various parameters, confusion may arise as to at what rate tax is to be deducted (S.195 for NR or other provisions applicable for Resident individuals)

RELIEF MEASURES ANNOUNCED UNDER COVID 19:-

With the outbreak of COVID 19 in India and the suspension of international flights on 22nd March, 2020 and declaration of lockdown in India and many other countries, many Non-Residents were forcefully bound for an extended stay in India. Hence, a relief circular was issued by CBDT on 8th May, 2020 (Circular No.11/2020) for granting a relief corresponding to FY 2019-20. In this circular, it was stated that for the computation of period of stay in India, such period shall be ignored if it pertains to

- Inability to leave India (period between 22.03.2020 to 31.03.2020)

- Departure on evacuation flight on or before 31.03.2020 (period between 22.03.2020 to date of departure)

- Departure before 31.03.2020 or has been stuck in India as on 31.03.2020 due to quarantine in India post 01.03.2020 (Period from 01.03.2020 to the date of departure or 31.03.2020)

CBDT via Circular No. 2/2021 dated 3rd March, 2021 has concluded that since OECD as well as most of the countries have clarified that in view of the provisions of the domestic income tax law read with the DTAAs, there does not appear a possibility of double taxation of income for PY 2020-21. However, in order to understand the possible situations in which a particular tax payer is facing double taxation due to forced stay in India, he may furnish the information in Form-NR which can be submitted electronically to the Principal Chief Commissioner of Income Tax (International Taxation). Hence no relief measures have been announced yet for FY 2020-21.

RESIDENTIAL STATUS OF INDIVIDUAL AS PER FOREIGN EXCHANGE MANAGEMENT ACT:

Residential status as per FEMA, 1999 is determined by the number of days in India in the preceding financial year (FY) and / or his purpose of stay. As per S. 2(v) of FEMA, 1999, any individual shall be considered as resident under FEMA if he resides in India for more than 182 days during the course of the preceding financial year. There are two exceptions in clause (A) and (B) which provides that even if an individual is resident due to his presence in India for more than 182 days in the preceding year, still he be a non-resident if he satisfies conditions mentioned in any of the exceptions in the Clauses. Clause (A) is for persons leaving India and Clause (B) is for persons coming to India.

Clause (A) Persons leaving India:-

If a person leaves India for any of the understated purposes, he will not be a Resident in India:-

- For taking up employment outside India; OR

- For carrying on any business outside India; OR

- For any purpose which indicates his intention of stay outside India for an uncertain period. Clause (B) Persons coming to India:-

- If a person comes to India for any of the understated purposes, he will be a Resident in India:-

- For taking up employment in India; OR

- For carrying on any business in India; OR

- For any purpose which indicates his intention of stay in India for an uncertain period.

Clause (B) is trickily worded in the Act. There is an exception to an exception. Hence, a person will be Resident in India if he comes to India for the above-mentioned purposes.

Hence, a person is said to be resident in India if he has resided in India for more than 182 days during the preceding FY and

- He has gone out of India for purpose other than employment outside India / other than business or vocation outside India / for a certain period or

- He has come for employment in India / for carrying business or vocation in India/ for an uncertain period.

So, when a person comes to India for a purpose other than employment / business or vocation / for an uncertain period, he shall be a person resident outside India irrespective of the number of days his stay in India in the preceding PY.

Similarly when a person goes out of India for the purpose of employment / business or vocation / for an uncertain period, he shall be a resident outside India irrespective of the number of days of his stay in India in the preceding PY.

A mere intention does not determine the residential status of the individual. When a person has come for employment or business in India, he is a resident. This is a fact and has nothing to do with intention. Intention comes into picture only when he comes to India under any other situation. But there also his intention to go back has to be supported by the facts.

Now let’s look at the key differences between the Residential Status under the ITA and FEMA:

| Income Tax Act, 1961 | FEMA, 1999 |

| Income Tax Act is a Revenue Law | FEMA is a Regulatory Law |

| Governs the taxability of income and tax thereon | Regulates the permissibility of financial and investment transactions |

| Residential Status is checked at the time of filing of Return of Income | Residential Status is checked at the time of entering into every financial transaction |

| No approval is required to earn income in India by NRs (except illegal activities) | Approval is required to undertake the financial transactions |

| Residential Status is decided based on stay in India | Residential Status is decided based on purpose of stay in India |

Hence due to different definitions under ITA and FEMA, there could be circumstances where person can be a resident under ITA and non-resident under FEMA. Let us try to decode this with the help of an example:-

Eg.1:- Mr.A is a resident Indian who takes up a job in USA in November 2020. He was in India before November, 2020. In this case, Mr. A has become Non-resident under FEMA from November, 2020 onwards regardless of the number of days of stay in India in FY 2019-20. However, under Income Tax Act, he will still be a resident for FY 2020-21 since he was in India for more than 182 days. Accordingly, his salary from Nov’20 to Mar’21 will be taxable in India subject to relief under DTAA. Hence an individual can have dual residency under FEMA but not in ITA.

Eg.2:- Mr. A is a NRI having FCNR fixed deposits. He returns to India in Nov’20. Under FEMA, he will become a Resident from Nov’20. However under ITA, he will still be a NR in FY 20-21 since his stay in India in the preceding 4 PYs is less than 365 days.

Under FEMA, Mr. A can continue to hold his FCNR deposits upto maturity. However for ITA, the interest on such FCNR deposits will be taxable since he is a resident under FEMA and hence the relief of exemption u/s 10(4)(ii) cannot be availed.

Impact of NRI status under FEMA:-

- Once the residential status changes to NRI under FEMA, he must visit all his banks, brokers and wealth managers to change his residential status from Resident to Non-Resident.

- A NRI cannot hold savings bank account. Hence on change of residential status to NRI under FEMA, he will need to open a NRO (Non-Resident Ordinary Rupee) account. NRO account can be jointly held by 2 or more NRIs. Only inward remittance from outside India is possible in NRO account and are non-repatriable to another country.

- NRI can also open NRE (Non-Resident External Rupee) account. NRE account permits money transfer services from outside India and the entire amount can be repatriated back to the country of residence of the NRI. Income earned in this account is exempt from tax.

- NRIs are permitted to enter into financial transactions only post approval from RBI.

CONCLUSION:-

Both Income Tax Act and FEMA are important laws deciding the residential status. Hence one should check the residential status from both taxation point of view and for every transaction to assess the requirement of RBI approvals.