Compounding: Most Desired; Least Achieved

Albert Einstein is reputed to have said: “Compound interest is the 8thwonder of the world. He who understands it earns it – he who doesn’t, pays it”.

The latter part of the above quote has been mysteriously forgotten and for as the quote was told over and over again, compound interest became the 8thwonder, but how only a few know.

Understanding compound interest can transform your life and help you exponentially in achieving your financial independence.

We have framed this article in sixparts:

- How Compounding Works

- Interest Rate Expectations

- Period of Investments

- Income vs Wealth

- Common Mistakes

- Conclusion

1. How Compounding Works:

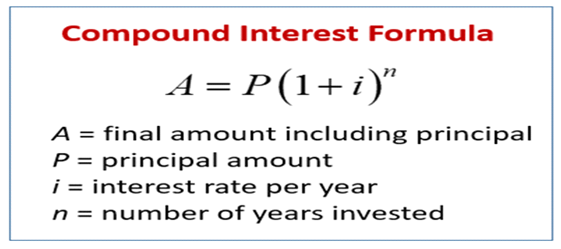

Compound interest is the interest on capital calculated based on both the initial principal and the accumulated interest from previous periods. Here’s the formula for annualized compound interest.

There are three main parts to this formula i.e. principal capital, rate of interest and length of the period, which we will discuss in a little depth. Let us first understand how compounding works.

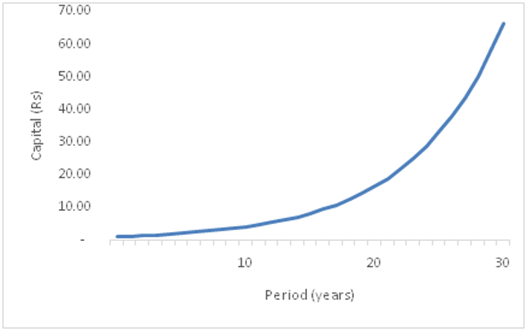

Following is the graph for 30 years of tenor @15% CAGR.

Money doubles every 5 years @15% CAGR. Over the 30 years, we have 6 blocks of 5 years which means money becomes 64x times (2^6).

- Most of the 64x comes in the later part of the journey, which means the tenor i.e. “n” in the above formula is a very important variable for compounding to work wonders. The longer you remain invested steeper the wealth will grow.

- Compounding assumes reinvestment i.e., all the returns earned are reinvested at the same rate and there are no withdrawals.

- Higher the rate of interest, steeper the curve and vice versa.

It is a process that starts from an initial state of small significance and builds upon itself, becoming larger.

1. Interest Rate Expectations:

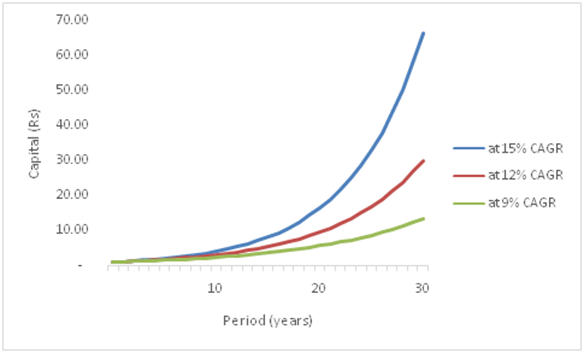

After you have understood how compounding works, the next step in thinking involves what and how interest rate expectations can be set to achieve our target wealth. Let us now assume 3 scenarios with equal principal, equal period but different interest rates.

There are various asset classes available such as equities, debt instruments, fixed deposits, gold, currencies, real estate, insurance products, etc. which can provide different investment returns based on different and unequal risk attached to it.

Every asset class has a journey and pace of growth of its own, only if you remain invested in them for a long period of time. Depending upon what your goals are based on your risk, you must choose these assets for investment. This is the most important aspect of compounding.

- Every incremental 1% adds great value to the power of compounding

- A person @15% takes 30 years to make as much as a person @12% in 37 years

To achieve wealth target taking benefit of compounding, the crux of the calculation above is investment CAGR, which is a different skillset in itself, which involves right asset allocation by managing risk with individual behavioral mindset. Also asset allocation needs to be seen from inflation angle too i.e. maintaining and increasing the purchasing power over a period of time.

Choosing a right asset and then ensuring that asset delivers as per the expectations is very crucial to achieving the power of compounding.

2. Period of Investment:

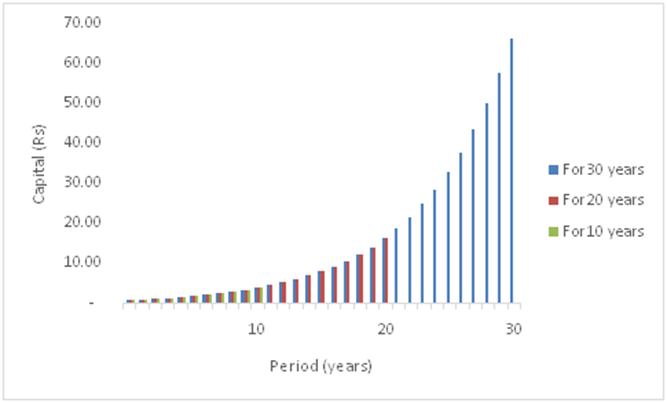

Now, this variable is something, which not everyone has the luxury to. We will show you how period is important in compounding. Let us assume 3 scenarios, with different periods, but same interest rates.

This shows that if a person starts the process of compounding early in life, they can achieve much more that what their peers can. Starting early can give you a little breather / luxury to tone down CAGR to achieve similar targets.

1. Income vs Wealth:

Let us now try to correlate how an individual can take benefit of compounding (with above average CAGR) to achieve what he is otherwise trying to achieve in his normal course of life. We assume achieving a 10% CAGR is doable and most of us achieve it, while achieving a 14% CAGR (we call it above average CAGR) is something people should be looking at.

Most of us focus more on Income generation (mainly salaried and professionals) so much that we don’t focus with equal seriousness on Wealth generation. Let us assume there are 2 categories of people i.e. one with decent wealth but focusing more on Income, and other category with equal wealth but focusing more on wealth. (Ignoring people with nominal or zero existing wealth whose only choice is to focus on Income before they can even start thinking to multiplying their wealth).

This is a very critical discussion and there lies a thin line of difference to accept the meaning out of it.

Below is the comparison of the two categories assuming income generators earn more sweat earnings while wealth generators earn a higher CAGR, given their aptitude, attitude, risk appetite and skillsets towards each of them.

| Particulars | Income Generators | Wealth Generators |

| Starting Wealth Invested | 2 crores | 2 crores |

| Investment CAGR | 10% | 14% |

| Period of evaluation | 30 years | 30 years |

| Value of Wealth at 30th year (A) | 34.90 crores | 101.90 crores |

| Long Term Average Sweat Earnings (Savings) | 25 lac p.a. | 10 lac p.a. |

| Sweat Money Accumulation at30th year (Cumulatively Reinvested at same rate) (B) | 45.24 crores | 18.09 crores |

| Total Individual Wealth (A+B) | 80.14 crores | 119.99 crores |

| Wealth Differentials | – | ~50% higher |

| Assumptions: Risk Appetite | Low | Moderate |

Now if you can plant these numbers on an excel sheet and accordingly tweak it w.r.t. your own scenarios, you shall figure out, how wealth generators can lead income generators by a mile. For you, to feature under the league of wealth generators, you need to ensure the following:

- Most of us sweat for money; then why not consider this math seriously.

- Most prefer the first route because income generators like stability (hate volatility and uncertainties), consider 14-15% CAGR as an uphill task (which it is, but not unachievable)

- Get to know how to achieve compounding at above average CAGR; then take steps towards achieving it.

- Sweat money once accumulated upto a particular corpus (say after initial 10 years of working) should then be compounded at above average CAGR. (around 15%)

Have you wondered why most of us are only concerned about a 10% hike in salaries and bonuses, and never bothered how growth in wealth can more than cope up with our salaries / profession? I think the answer to this is urge for stability in cash flows letting go of the upside in wealth!

In the above examples we have considered wealth generators to achieve above average CAGR i.e. in the range of 14% CAGR because that much ROI is required for this option to be attractive. While the real CAGR for every year may be volatile, what matters is achieving this CAGR over a longish period of time, which in our opinion is very much POSSIBLE.

Two things to consider if you belong to income generators league:

- In wealth management activity, we can definitely ensure wealth grows steadily over a period of time (though not on annual basis if evaluated)

- Also, income generation activity carries risks too, which we don’t measure as much as we measure and fear wealth growing activities.

All this debate revolves around achieving that additional and high impactful 300-400bps or so in our wealth performance, which can be achieved with higher skills and planned strategies.

2. Common Mistakes:

While compounding of returns is something which most of us dream of, only a few (may be ~5% of us) would be able to achieve them. We list down few mistakes which people commit to when they venture with their wealth management activities:

- People acquire skill sets to feature under first route (income generation), but have no endeavor to acquire any skill sets to feature under second route (wealth generation).

- People assume compounding to be a linear straight line, and hence wrong expectations are set in leading to disappointments.

- People are so OKAY to lose money or under perform in their wealth management activities; while income generation gets full focus and energy.

- Greed and fear take more control over investment decisions, than sanity of mind.

- Inability to handle volatility and unstable compounding; let alone take advantage of them.

- It’s always said investment journey is a lonely one; while most of us follow herd mentality. People have to realize and strategize their own strategy and investment counters well, which will differ from their peers.

- Some people often mistake compounding with gamble i.e. they don’t want to give enough time to it, but want equal results quickly. Such people must put their aggression to best use.

With the above reasons, most of us falter in the pursuit to compound returns.

3. Conclusion:

Compounding of returns is indeed very magical and a very sharp tool to increase our wealth manifold. While it looks easy, it is indeed a difficult task to achieve the target. Few points we would like to mention:

- Many are born with legacy wealth, start early and try maintaining the CAGR as high as possible and the job is done.

- Compounding is a zig zag line which requires planning, preparedness and capability to set up investment strategies.

- Learn to deal with instability and volatility because that’s the key to achieving compounding

- Patience is key.To reduce the target period, don’t take hasty steps

- Know what investment assets suits you; when mindset is not the one that can handle risk, avoid it.

- Avoid herd; avoid momentum

- You have to do something different, to achieve something different (higher)

Compounding is like a philosopher’s stone which in ordinary in looks, easy to understand, can generate gold out of anything but when it comes to maintaining emotional discipline many people lack in that.These profound concepts about compounding can be applied while investing, while carrying out business activities and in other aspects of life too. Unleash this beast and let it reap the benefits for you.