SA 230: Audit Documentation

Documentation is considered the backbone of an audit. The work that the auditor performs, the explanations given to the auditor, the conclusions arrived at, all are evidenced by documentation. Inadequate or improper documentation may be considered as deficiency in performing an audit. The auditor may have executed appropriate audit procedures, however, if there is no documentation to prove, it may put question on the work done, in case any material misstatement is reported and may put the auditor in difficult situations, such as penal actions from various regulators.

The focus of National Financial Reporting Authority (‘NFRA”) since it was set up has been on maintenance of Audit Quality. It has been coming hard on auditors for non-compliance with SAs, Laws, Regulations, etc. highlighted after extensive reviews of documentation maintained by the auditors.

Maintaining sufficient and appropriate audit documentation is of utmost importance in today’s time. The regulator, NFRA, is focused on automation and digitally maintenance of such audit documents. NFRA has also been exploring to set up Digi Locker facility for audit documentation so that the documents once finalised cannot be amended after the date of the audit report.

So, what is the objective of Audit Documentation? The objective is for the auditor to prepare documentation that provides: (a) a sufficient and appropriate record of the basis for the auditor’s report; and (b) evidence that the audit was planned and performed in accordance with SAs and applicable legal and regulatory requirements.

Documentation is essential because:

- It supports the auditor’s basis for an audit finding

- Provides evidence that audit was planned and performed

- It assists supervision and review

- It results in better conceptual clarity, clarity of thought and expression

- It facilitates better understanding and helps avoid misconception

- It supports and evidences compliance with standards on auditing, applicable legal & regulatory requirements

Documentation of the Audit Procedures Performed and Audit Evidence Obtained

Form, Content and Extent of Audit Documentation

The auditor shall prepare audit documentation that is sufficient to enable an experienced auditor, having no previous connection with the audit, to understand:

(a) The nature, timing, and extent of the audit procedures performed to comply with the SAs and applicable legal and regulatory requirements;

(b) The results of the audit procedures performed, and the audit evidence obtained; and

(c) Significant matters arising during the audit, the conclusions reached thereon, and significant professional judgments made in reaching those conclusions.

In documenting the nature, timing and extent of audit procedures performed, the auditor shall record:

(a) The identifying characteristics of the specific items or matters tested;

(b) Who performed the audit work and the date such work was completed; and

(c) Who reviewed the audit work performed and the date and extent of such review.

The auditor shall document discussions of significant matters with management, those charged with governance, and others, including the nature of the significant matters discussed and when and with whom the discussions took place.

If the auditor identified information that is inconsistent with the auditor’s final conclusion regarding a significant matter, the auditor shall document how the auditor addressed the inconsistency.

If, in exceptional circumstances, the auditor judges it necessary to depart from a relevant requirement in a SA, the auditor shall document how the alternative audit procedures performed achieve the aim of that requirement, and the reasons for the departure.

Ownership of Audit Documentation:

Standards on Quality Control (SQC 1) provides that, unless otherwise specified by law or regulation, audit documentation is the property of the auditor.

He may at his discretion, make portions of, or extracts from, audit documentation available to clients, provided such disclosure does not undermine the validity of the work performed, or in case of assurance engagements, the independence of the auditor or of his personnel.

Assembly of the Final Audit File

The Auditor shall assemble the audit documentation in an audit file on a timely basis.

SQC 1 requires firms to establish policies and procedures for the timely completion of assembly of audit files and the retention period of engagement documentation.

An appropriate time limit within which to complete the assembly of the final audit file is ordinarily not more than 60 after the date of the auditor’s report.

After the assembly of the final audit file, the auditor shall not delete or discard audit documentation.

The retention period of audit engagements should not be shorter than 7 years from the date of the auditor’s report, or if later, the date of the group’s auditor’s report.

There is a definite shift in focus of auditors from traditional audit methods to more specific approach as mentioned in the SAs with appropriate documentation. With the rising expectations of the regulators pertaining to maintenance of audit documentation, CA firms are increasingly adopting audit documentation softwares that would enable them to time-stamp and properly store the audit documents. This would help in contemporaneous audit documentation with adequate detail during the course of the audit itself.

SA 250: Consideration of Laws and Regulations in an Audit of Financial Statements

This Standard on Auditing (SA) deals with the auditor’s responsibility to consider laws and regulations when performing an audit of financial statements. This SA does not apply to other assurance engagements in which the auditor is specifically engaged to test and report separately on compliance with specific laws or regulations.

Responsibility of Management for Compliance with Laws and Regulations:

It is the responsibility of management, with the oversight of those charged with governance, to ensure that the entity’s operations are conducted in accordance with the provisions of laws and regulations, including compliance with the provisions of laws and regulations that determine the reported amounts and disclosures in an entity’s financial statements.

Responsibility of the Auditor

The auditor is responsible for obtaining reasonable assurance that the financial statements, taken as a whole, are free from material misstatement, whether caused by fraud or error. In conducting an audit of financial statements, the auditor takes into account the applicable legal and regulatory framework. Owing to the inherent limitations of an audit, there is an unavoidable risk that some material misstatements in the financial statements may not be detected, even though the audit is properly planned and performed in accordance with the SAs.

Requirements:

As part of obtaining an understanding of the entity and its environment in accordance with SA 315, the auditor shall obtain a general understanding of: (a) The legal and regulatory framework applicable to the entity and the industry or sector in which the entity operates; and (b) How the entity is complying with that framework.

The auditor shall obtain sufficient appropriate audit evidence regarding compliance with the provisions of those laws and regulations generally recognised to have a direct effect on the determination of material amounts and disclosures in the financial statements.

The auditor shall perform the following audit procedures to help identify instances of non-compliance with other laws and regulations that may have a material effect on the financial statements:

(a) Inquiring of management and, where appropriate, those charged with governance, as to whether the entity is in compliance with such laws and regulations; and

(b) Inspecting correspondence, if any, with the relevant licensing or regulatory authorities

Audit Procedures When Non-Compliance is Identified or Suspected:

If the auditor becomes aware of information concerning an instance of non-compliance or suspected non-compliance with laws and regulations, the auditor shall obtain:

- An understanding of the nature of the act and the circumstances in which it has occurred; and

- Further information to evaluate the possible effect on the financial statements.

If the auditor suspects there may be non-compliance, the auditor shall discuss the matter with management and, where appropriate, those charged with governance. If management or, as appropriate, those charged with governance do not provide sufficient information that supports that the entity is in compliance with laws and regulations and, in the auditor’s judgment, the effect of the suspected non-compliance may be material to the financial statements, the auditor shall consider the need to obtain legal advice.

Indications of Non-Compliance with Laws and Regulations:

- Investigations by regulatory organisations and government departments or payment of fines or penalties.

- Purchasing at prices significantly above or below market price.

- Unusual payments in cash, purchases in the form of cashiers’ cheques payable to bearer or transfers to numbered bank accounts.

- Unusual payments towards legal and retainership fees

- Payments without proper exchange control documentation.

- Existence of an information system which fails, whether by design or by accident, to provide an adequate audit trail or sufficient evidence.

- Unauthorised transactions or improperly recorded transactions.

Reporting of Identified or Suspected Non-Compliance

Reporting Non-Compliance to Those Charged with Governance

Unless all of those charged with governance are involved in management of the entity, and therefore are aware of matters involving identified or suspected non-compliance already communicated by the auditor, the auditor shall communicate with those charged with governance matters involving non-compliance with laws and regulations that come to the auditor’s attention during the course of the audit, other than when the matters are clearly inconsequential.

Reporting Non-Compliance in the Auditor’s Report on the Financial Statements

If the auditor concludes that the non-compliance has a material effect on the financial statements, and has not been adequately reflected in the financial statements, the auditor shall, in accordance with SA 705(Revised)6 , express a qualified or adverse opinion on the financial statements.

Reporting Non-Compliance to Regulatory and Enforcement Authorities

If the auditor has identified or suspects non-compliance with laws and regulations, the auditor shall determine whether the auditor has a responsibility to report the identified or suspected non-compliance to parties outside the entity.

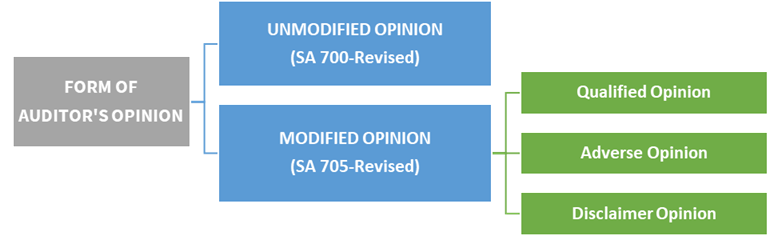

The Auditor’s Report on Financial Statements – SA 700/705/706 (Revised)

An Auditor’s Report is the final outcome of any audit process. The importance of an Auditor’s Report in developing stakeholders’ confidence on the correctness and reliability of financial statements cannot be under-stated.

SA 700 (Revised) deals with the auditor’s responsibility to form an opinion on the financial statements and provides the form and content of the Auditor’s Report. SA 705 (Revised) and SA 706 (Revised) deals with form and content of Modified Opinion, Emphasis of Matter and Other Matter paragraphs.

Requirements under SA 700 (Revised)

The auditor shall form an opinion on whether the financial statements are prepared in all material respects, in accordance with the applicable Financial Reporting Framework (‘FRF’) and provide reasonable assurance about whether the financial statements are free of material misstatement due to fraud or error. This opinion is formed based on an evaluation of sufficient appropriate audit evidence and qualitative aspects of the entity’s accounting practices, including indicators of possible bias in management’s judgements.

The auditor’s evaluation of financial statements should assess the following areas:

- Application and disclosure of significant accounting policies.

- Consistency of accounting policies with the applicable FRF.

- Reasonableness of accounting estimates.

- Whether information presented is relevant, reliable, comparable and understandable.

- Adequacy of disclosures to enable the users to understand the effect of material transactions.

- Use of appropriate terminology in the financial statements.

Basic Elements of an Auditor’s Report:

- Title: The auditor’s report shall have a title that clearly indicates that it is the report of an independent auditor.

- Addressee: The auditor’s report shall be addressed, as appropriate, based on the circumstances of the engagement.

- Opinion: The first section of the auditor’s report shall include the auditor’s opinion, and shall have the heading “Opinion”. If the applicable FRF are not the accounting standards issued by ICAI, ASB, etc. then the auditor shall identify the relevant jurisdiction.

- Basis for Opinion: The “Basis for Opinion” shall directly follow the Opinion section. The Basis of Opinion shall state that the audit was conducted in accordance with Standards on Auditing, describe auditor’s responsibilities under the SAs, include a statement on the auditor’s independence and state whether the auditor has obtained sufficient and appropriate audit evidence to form an opinion

- Going Concern: Where applicable, the auditor shall report in accordance with SA 570 (Revised) ‘Going Concern’.

- Key Audit Matters: For audits of complete set of general purpose financial statements of listed entities, or otherwise as may be required by law or regulation or necessity, the auditor shall communicate Key Audit Matters in the auditor’s report in accordance with SA 701.

- Responsibilities for the Financial Statements: This section shall explicitly describe the management’s responsibility for the: (i) preparation and presentation of financial statements in accordance with applicable FRF; (ii) design, implementation and maintenance of internal controls necessary to ensure that financial statements are free from material misstatements due to fraud and error; (iii) assessment of entity’s ability to continue as a going concern.

- Auditor’s Responsibilities for the Audit of the Financial Statements: Under this section, the auditor shall clearly state that the objective of the audit is to obtain a reasonable assurance (i.e., a high level of assurance but not a guarantee) about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error and provide an opinion thereon.

The following key statements are required to be made under this section to adequately convey an auditor’s responsibility towards the financial statements:

- State that the auditor exercises professional judgment and maintains professional skepticism throughout the audit

- Describe the activities carried out as a part of the audit such as: (i) identification and assessment of risks of material misstatement, (ii) understanding of internal controls, (iii) appropriateness of accounting policies and reasonableness of accounting estimates & related disclosures made by management, (iv) appropriateness of the management’s use of the going concern basis of accounting and (v) evaluation of whether the financial statements achieve fair presentation

- Communication with TCWG regarding: (i) planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control identified during the audit, (ii) compliance with ethical requirements regarding independence and (iii) Key Audit Matters, wherever considered significant.

The desired wordings for the above are provided in SA 700 (Revised) and auditors must take due care in including these statements and/or declarations in the auditor’s report.

- Other Reporting Responsibilities: If the auditor addresses other reporting responsibilities in the auditor’s report on the financial statements that are in addition to the auditor’s responsibilities under the SAs, these other reporting responsibilities shall be addressed in a separate section in the auditor’s report with a heading titled “Report on Other Legal and Regulatory Requirements”. For example: Section 143(11) of the Companies Act, 2013 requires specific reporting under Companies (Auditors’ Report) Order, 2020.

- Signature of the Auditor: The report is signed by the auditor (i.e., the engagement partner) in his personal name. Where the firm is appointed as the auditor, the report is signed in the personal name of the auditor and in the name of the audit firm. The partner/proprietor signing the audit report also needs to mention the membership number assigned by the ICAI along with the registration number of the firm as allotted by ICAI.

- Place of Signature: The auditor’s report shall name specific location, which is ordinarily the city where the audit report is signed.

- Date of the Auditor’s Report: The auditor’s report shall be dated no earlier than the date on which the auditor has obtained sufficient appropriate audit evidence on which to base the auditor’s opinion on the financial statements.

SA 705 (Revised): Modification to the opinion in the Independent Auditor’s Report

The auditor shall modify the opinion in the auditor’s report when:

- The auditor concludes that, based on the audit evidence obtained, the financial statements as a whole are not free from material misstatement; or

- The auditor is unable to obtain sufficient appropriate audit evidence to conclude that the financial statements as a whole are free from material misstatement.

- Use the heading – “Qualified Opinion”, “Adverse Opinion”, or “Disclaimer of Opinion”

- Must use the phrases – “with the foregoing explanation” or “subject to” or “except that”

Qualified Opinion:

- The auditor shall express qualified opinion when he concludes that the misstatements, individually or in aggregate are material but not pervasive* to the financial statements or he is unable to obtain sufficient appropriate audit evidence but also concludes that the possible effects of undetected misstatements could be material but not pervasive*.

- Where a qualified opinion is issued due to material misstatement the auditor shall state in the opinion paragraph that except for the matters described in the basis of qualified opinion, the financial statements have been prepared, in all material respects, in accordance with the applicable FRF. When modification arises from inability to obtain sufficient appropriate audit evidence, the auditor shall use the corresponding phrase “except for the possible effects of the matter(s)…” for the modified opinion.

Adverse Opinion:

- When the auditor concludes that having obtained sufficient appropriate audit evidence, the misstatements, individually or in aggregate, are both material and pervasive*, he issues an adverse opinion.

- When issuing an adverse opinion, the auditor shall state:

- That the financial statements DO NOT PRESENT a true and fair view; or

- The financial statements have NOT been prepared, in all material respects, in accordance with the applicable FRF.

Disclaimer Opinion:

- When the auditor is unable to obtain sufficient appropriate audit evidence and concludes that the possible effects of undetected misstatements are both material and pervasive*, he issues a Disclaimer of Opinion.

- In extremely rare circumstances, having obtained sufficient appropriate audit evidence, but due to multiple uncertainties, the auditor is unable to form an opinion, due to possible interaction of those uncertainties and their possible outcomes, he issues a Disclaimer of Opinion.

- When the auditor disclaims an opinion due to inability to obtain sufficient appropriate audit evidence, he shall state that due to the significance of the matter(s) described in the Basis for Disclaimer of Opinion paragraph, the auditor has not been able to obtain sufficient appropriate audit evidence and does not express an opinion on the financial statements.

To summarise:

| Particulars | Modified Opinion | ||

| Qualified Opinion | Adverse Opinion | Disclaimer of Opinion | |

| Misstatements individually or in aggregate | Material but not Pervasive | Both Material and Pervasive | Both Material and Pervasive |

| Unable to obtain SAAE to base opinion and possible effects on FS of undetected misstatements | Material but not Pervasive | Both Material and Pervasive | Both Material and Pervasive |

(*) Pervasive – A term used, in the context of misstatements, to describe the effects on the financial statements of misstatements or the possible effects on the financial statements of misstatements, if any, that are undetected due to an inability to obtain sufficient appropriate audit evidence. Pervasive effects on the financial statements are those that, in the auditor’s judgment:

- Are not confined to specific elements, accounts or items of the financial statements;

- If so confined, represent or could represent a substantial proportion of the financial statements; or

- In relation to disclosures, are fundamental to users’ understanding of the financial statements.

SA 706 (Revised) – Emphasis of Matter and Other Matter Paragraphs in the Independent Auditor’s Report

Emphasis of Matter Paragraph in the Auditor’s Report

If the auditor considers it necessary to draw users’ attention to a matter presented or disclosed in the financial statements that, in the auditor’s judgment, is of such importance that it is fundamental to users’ understanding of the financial statements, the auditor shall include an “Emphasis of Matter” paragraph in the auditor’s report provided the auditor has obtained sufficient appropriate audit evidence that the matter is not materially misstated in the financial statements. Such a paragraph shall refer only to information presented or disclosed in the financial statements.

When the auditor includes an Emphasis of Matter paragraph in the auditor’s report, the auditor shall:

(a) Include it immediately after the Opinion paragraph in the auditor’s report;

(b) Use the heading “Emphasis of Matter”, or other appropriate heading;

(c) Include in the paragraph a clear reference to the matter being emphasised and to where relevant disclosures that fully describe the matter can be found in the financial statements; and

(d) Indicate that the auditor’s opinion is not modified in respect of the matter emphasised.

Example of para to be given in Audit Report:

Emphasis of Matter – Effects of a Fire (Heading)

We draw attention to Note X of the financial statements, which describes the effects of a fire in the Company’s production facilities. Our opinion is not modified in respect of this matter.

Other Matter Paragraph in the Auditor’s Report

If the auditor considers it necessary to communicate a matter other than those that are presented or disclosed in the financial statements that, in the auditor’s judgment, is relevant to users’ understanding of the audit, the auditor’s responsibilities or the auditor’s report and this is not prohibited by law or regulation, the auditor shall do so in a paragraph in the auditor’s report, with the heading “Other Matter”. The auditor shall include this paragraph immediately after the Opinion paragraph and any Emphasis of Matter paragraph, or elsewhere in the auditor’s report if the content of the Other Matter paragraph is relevant to the Other Reporting Responsibilities section.

Example of para to be given in Audit Report:

Other Matter

We did not audit the financial statements/ information of XX (number) branches included in the standalone financial statements of the Company whose financial statements/financial information reflect total assets of Rs. XX as at 31st March 20XX and the total revenue of Rs. XX for the year ended on that date. The financial statements/information of these branches have been audited by the branch auditors whose reports have been furnished to us, and our opinion in so far as it relates to the amounts and disclosures included in respect of these branches, is based solely on the report of such branch auditors. Our opinion is not modified in respect of these matters.

SA 701: ‘Communicating Key Audit Matters in Independent Auditor’s Report’

Applicability & Purpose of SA 701:

This SA applies to:

- audits of complete sets of general purpose financial statements of listed entities;

- circumstances when the auditor otherwise decides to communicate key audit matters in the auditor’s report;

- cases whether the auditor is required by law or regulation to communicate key audit matters in the auditor’s report

However, SA 705 (Revised) prohibits the auditor from communicating key audit matters when the auditor disclaims an opinion on the financial statements unless such reporting is required by law or regulation.

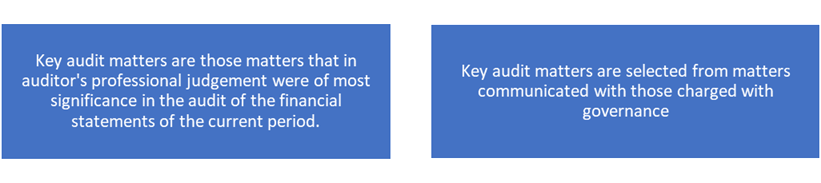

The purpose of communicating key audit matters is to enhance the communicative value of the auditor’s report by providing greater transparency about the audit that was performed. Communicating key audit matters provides additional information to intended users of the financial statements (“intended users”) to assist them in understanding those matters that, in the auditor’s professional judgment, were of most significance in the audit of the financial statements of the current period.

Some examples of Key Audit Matters:

- Assessment of impairment

- Provision for losses and contingencies

- Valuation of financial instruments

- Matters relating to revenue recognition

- Taxation matters (existence of multiple tax jurisdictions, uncertain tax positions, deferred tax assets)

However, the auditor should ensure that communicating key audit matters in an audit report is not a substitution for any disclosures that the management has to make in the Financials Statements or a substitution to the reporting requirements under SA 700, SA 705 and SA 706 (Revised).

Communicating Key Audit Matters in Auditor’s Report:

An auditor should describe each of the key audit matter, with the help of a suitable sub-heading, in the separate section of his audit report under “Key Audit Matters”.

The introductory language in this section of the auditor’s report shall state:

- that key audit matters are those matters that, in the auditor’s professional judgment, were of most significance in the audit of the financial statements (of the current period) and

- How these matters were addressed in the context of the audit of the financial statements as a whole and in forming the auditor’s opinion thereon and that the auditor does not provide a separate opinion on these matters.

Communication with Person(s) Charged with Governance

The auditor should communicate with the person(s) charged with governance:

- Matters which the auditor considers key audit matters

- In case applicable, based on the circumstances and facts of the entity and the audit, the determination of the auditor that there aren’t any key audit matters for the purpose of communicating in his report

Documentation

During Documentation, the Auditor should document:

- Matters which required his significant attention as determined above, and the basis for his determination whether such matter is a key audit matter

- Where applicable, the basis for the auditor in determining that there aren’t key audit matters for the purpose of communicating in the auditor’s report

- Where applicable, the basis for the auditor in determining not to communicate in his/her report a matter which was considered to be a key audit matter

SA 710 (Revised): Comparative Information– Corresponding Figures and Comparative Financial Statements

This Standard on Auditing (SA) deals with the auditor’s responsibilities regarding comparative information in an audit of financial statements. When the financial statements of the prior period have been audited by a predecessor auditor or were not audited, the requirements and guidance in SA 510 regarding opening balances also apply.

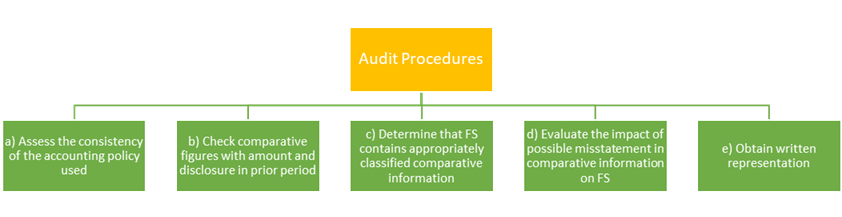

Audit Procedures

The auditor shall determine whether the financial statements include the comparative information required by the applicable financial reporting framework and whether such information is appropriately classified.

For this purpose, the auditor shall evaluate whether:

- The comparative information agrees with the amounts and other disclosures presented in the prior period; and

- The accounting policies reflected in the comparative information are consistent with those applied in the current period or, if there have been changes in accounting policies, whether those changes have been properly accounted for and adequately presented and disclosed.

The auditor shall request written representations for all periods referred to in the auditor’s opinion. The auditor shall also obtain a specific written representation regarding any prior period item that is separately disclosed in the current year’s statement of profit and loss.

Audit Reporting

Corresponding Figures:

Auditor’s opinion should refer to corresponding figures in the opinion only when:

- If the auditor’s report on the prior period, as previously issued, included a qualified opinion, a disclaimer of opinion, or an adverse opinion and the matter which gave rise to the modification is unresolved, the auditor shall modify the auditor’s opinion on the current period’s financial statements.

- If the auditor obtains audit evidence that a material misstatement exists in the prior period financial statements on which an unmodified opinion has been previously issued, the auditor shall verify whether the misstatement has been dealt with as required under the applicable financial reporting framework and, if that is not the case, the auditor shall express a qualified opinion or an adverse opinion in the auditor’s report on the current period financial statements, modified with respect to the corresponding figures included therein

- If the prior period financial statements were not audited, the auditor shall state in an Other Matter paragraph in the auditor’s report that the corresponding figures are unaudited. Such a statement does not, however, relieve the auditor of the requirement to obtain sufficient appropriate audit evidence that the opening balances do not contain misstatements that materially affect the current period’s financial statements.

Comparative Financial Statements

- When comparative financial statements are presented, the auditor’s opinion shall refer to each period for which financial statements are presented and on which an audit opinion is expressed.

- When reporting on prior period financial statements in connection with the current period’s audit, if the auditor’s opinion on such prior period financial statements differs from the opinion the auditor previously expressed, the auditor shall disclose the substantive reasons for the different opinion in an Other Matter paragraph in accordance with SA 706 (Revised).

- If the financial statements of the prior period were audited by a predecessor auditor, in addition to expressing an opinion on the current period’s financial statements, the auditor shall state in an Other Matter paragraph, that the financial statements of the prior period were audited by a predecessor auditor, The type of opinion expressed by the predecessor auditor and, if the opinion was modified, the reasons therefor and the date of audit report.

- If the prior period financial statements were not audited, the auditor shall state in an Other Matter paragraph that the comparative financial statements are unaudited.

SA 720: The Auditor’s Responsibility in Relation to Other Information in Documents containing Audited Financial Statements

This standard deals with auditors responsibilities relating to Other Information whether financial or non-financial, included in entity’s annual report.

Objectives of the Auditor

- Consider whether there is material inconsistency between other information and financial statements.

- Consider whether there is material inconsistency between other information and auditors’ knowledge obtained in the audit.

- Auditor should respond appropriately when he identifies material inconsistencies or when other information appears to be materially misstated.

Reporting requirements:

The auditor’s report shall include a separate section with a heading “Other Information”, or other appropriate heading, when, at the date of the auditor’s report.

When the auditor’s report is required to include an Other Information section in audit report, this section shall include:

- A statement that management is responsible for the other information;

- An identification of:

- Other information, if any, obtained by the auditor prior to the date of the auditor’s report; and

- For an audit of financial statements of a listed entity, other information, if any, expected to be obtained after the date of the auditor’s report;

- A statement that the auditor’s opinion does not cover the other information and, accordingly, that the auditor does not express (or will not express) an audit opinion or any form of assurance conclusion thereon;

- A description of the auditor’s responsibilities relating to reading, considering and reporting on other information as required by this SA; and

- When other information has been obtained prior to the date of the auditor’s report, either:

- A statement that the auditor has nothing to report; or

- If the auditor has concluded that there is an uncorrected material misstatement of the other information, a statement that describes the uncorrected material misstatement of the other information.

Example of para to be included in Audit Report:

Other Information

The Company’s Board of Directors is responsible for the other information. The other information comprises the [information included in the XXX report, but does not include the financial statements and our auditor’s report thereon.]

Our opinion on the financial statements does not cover the other information and we do not express any form of assurance conclusion thereon.

In connection with our audit of the financial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in the audit or otherwise appears to be materially misstated. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard.